Interest rates, in the dilemma between inflation and the exchange rate

Recently, for the second time this year, the European ...

Banka e Shqipërisë paralajmëroi këtë muaj për rreziqe të shtuara nga rritja e shpejtë e kreditimit të ekonomisë. Shqetësimet lidhen sidomos me rritjen e shpejtë të kredisë në pasuri të paluajtshme, ndërkohë që po vërehet edhe një rritje e oreksit për rrezik dhe e ekspozimeve të mëdha në segmentin e korporatave.

In the Declaration of Financial Stability for the first six months of the year, the Bank of Albania underlined for the first time, explicitly, the concern that lending to the economy this year is growing too fast and that it is necessary to slow down the pace of growth.

This increase can be explained by several essential factors, both on the demand side and on the supply side. Inflation during this year has suffered a significant decline and has been below the target of the Bank of Albania for months.

This development seems to have improved the confidence of the private sector of the economy and avoided the risk of a further increase in interest rates, and even created expectations in the opposite direction, for their reduction. The decision of the Bank of Albania to reduce the base rate to 3%, in July, has confirmed these expectations.

The performance of specific sectors of the economy, such as those related to tourism and real estate, continues to arouse optimism and new investment projects from businesses.

On the other hand, the readiness of the banking sector to give loans seems high, supported by the good state of the balance sheets and the improvement of the financial performance.

The increase in appetite for risk is also evidenced by the addition of large exposures to projects and special clients of the corporate segment. Meanwhile, exposure through lending in the real estate sector continues to grow, both for households and businesses.

However, this rapid growth initially raised the concern of the International Monetary Fund (IMF), which in January of this year warned the Bank of Albania about the risks of rapid credit growth, especially in the real estate segment.

The Bank of Albania reacted at the end of June, further increasing the requirements for the level of capital adequacy, through the application for the first time of a countercyclical rate, which has the direct purpose of curbing the rapid growth of lending.

The data of the Bank of Albania show that for the first 7 months of the year, the new loan has grown at high rates and remains at the highest level for at least the last nine years. In the January-July period, a total of 211 billion new loans were granted, with an increase of 30% more compared to the same period last year.

The rapid growth of credit this year is supported especially by business. Private companies received a total of 149.5 billion ALL in loans, with an increase of 44.5% compared to the same period last year.

Even the new loan for individuals in July continued the stable growth, reaching the value of 61.3 billion lek, an increase of 18% compared to the previous year. Lending to individuals continues to rely especially on the financing of real estate purchases.

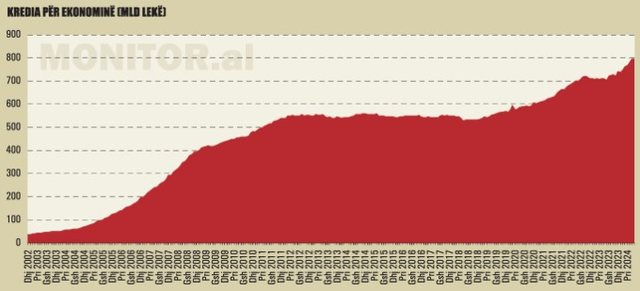

At the end of July, the total loan portfolio for the economy, expressed as a surplus, continued to grow. It reached the value of ALL 798.3 billion, 13.3% more compared to the previous year. Growth continues to be higher in the individuals segment, where the portfolio has reached the value of ALL 309 billion, increasing by 13.6% compared to a year ago.

While in the business segment, the value of the loan portfolio reached ALL 447.5 billion, increasing by 12.8% compared to the same period a year ago.

The Albanian banking sector is fresh from the experience of a rapid cycle of credit growth, which was followed by a strong increase in non-performing loans.

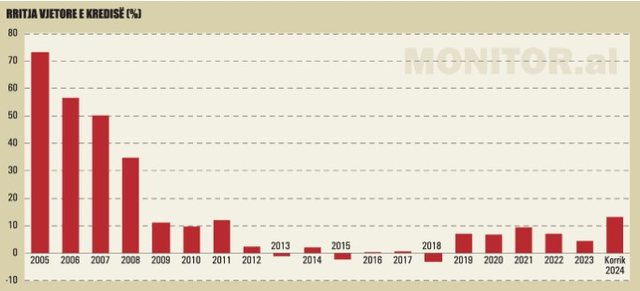

After the privatization of the Savings Bank and the entry into the market of Raiffeisen Bank, the Albanian economy entered the first cycle of very rapid credit growth. Credit took off very quickly in 2005, with an annual growth of 73%.

High growth rates continued to be very high until 2008, at almost 35%, while the following years slowed, but always remained in positive growth territory, until 2013. This moment coincided with the deepening of the crisis. of non-performing loans, which in 2014 would reach the level of 25%.

In the period 2013-2018, the loan portfolio moved between decline and stagnation, while a new cycle of real growth started only in 2019, even following the structural changes and consolidation of the banking sector.

Despite the recovery, credit growth never reached double-digit levels, also due to the restraint brought by the pandemic, due to the inflationary crisis and the increase in interest rates in 2022, but also the negative statistical effect of the appreciation of the Lek on the exchange rate.

But, this year, lending has taken off rapidly and reached double-digit levels. At the end of July, the annual growth of the loan portfolio reached 13.3%. This is the highest rate of credit growth since 2008.

At the moment, however, credit growth remains far from the levels of 2005-2008 (in the range of 35-73%), however, it must be said that the growth of that period started from a fairly low base.

However, if we analyze the credit segment that currently creates the main concerns for the Bank of Albania, that for real estate, the growth is much higher.

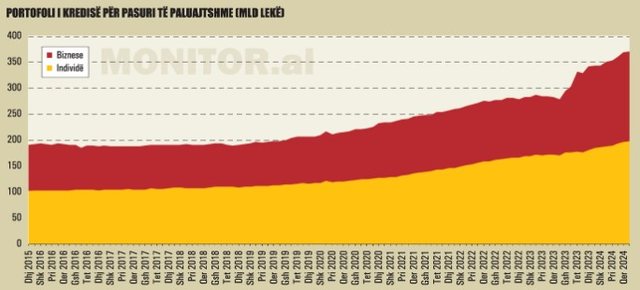

The exposure of the banking sector in loans for real estate has reached 371 billion ALL, or approximately 3.7 billion euros. According to Bank of Albania statistics, the total value of loans for real estate (nominal value, not adjusted for exchange rate changes) is increasing annually by 33%. This figure includes both customer segments, businesses and individuals.

The majority of the portfolio belongs to individuals, with approximately 53% of the total exposure in loans for real estate, while the difference of 47% is credit given to businesses.

However, the recent rapid increase in the size of the portfolio is mainly due to the business. For the last 12 months, the loan portfolio for business real estate has increased by 60%, while in the segment of individuals, by 16%.

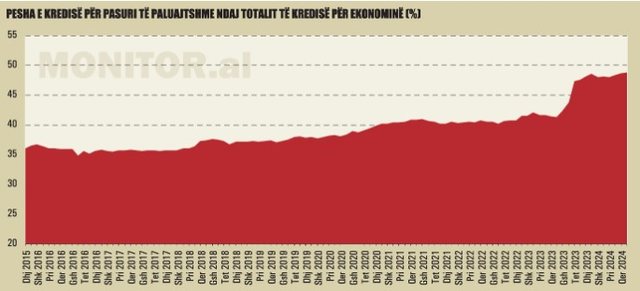

Currently, real estate loans for individuals and businesses make up about 49% of the total loan portfolio granted to the private sector of the economy.

In recent years, the banking sector has significantly increased the loan portfolio for properties, both for businesses and for individuals. It is estimated that lending has been a very important factor in supporting demand in the real estate market.

But, on the other hand, this has also increased the exposure of the banking sector against the performance of the real estate market.

In the vast majority of cases, loans for real estate are secured with properties left as collateral in favor of banks (in the most typical case, the property itself purchased with a loan). A potential crisis in the real estate market would reduce the value of collateral and expose banks to the risks of loan losses.

In October last year, the Bank of Albania approved the regulation "On data reporting, identification and monitoring of indicators on lending and investments for real estate".

According to the Bank of Albania, this regulation formalizes, standardizes and expands the data collected by banks and lending entities regarding the indicators of the standards they use for exposure to residential and commercial real estate.

Also, the regulation offers the possibility for the Bank of Albania to use these indicators as macroprudential policy instruments, when it is necessary to mitigate the risks associated with these exposures if they are assessed at high levels.

In the case of residential real estate loans, lending entities must provide the necessary details and classifications of data for each such loan in order to identify and monitor indicators of their exposure to the residential real estate market. .

In case real estate lending seems to be the most "overheated" segment of lending, another indicator of the fact that the banking sector is showing a growing appetite for risk is the increase in financing in the corporate segment.

According to the data of the Bank of Albania, the loan for large business at the end of July reached the value of 234.6 billion ALL, an increase of 21.5% compared to the same period of the previous year.

This growth rate is significantly higher compared to the average growth of the loan portfolio for the economy (13.3%) and the average growth of the business portfolio (12.8%).

The detailed data show that the highest rate of loan growth for large business is registered in the segment of long-term loans, which usually aim to finance new investment projects. Long-term credit at the end of July resulted in annual growth of more than 34%.

The increase in credit for corporations also includes exposures of quite large values ??to specific borrowers, which in some cases are being given in cooperation between banks, using the instrument of syndicated loans.

This summer, four Albanian commercial banks have signed with Ayen AS Energji the contract with the largest syndicated loan in the history of the Albanian banking sector.

Raiffeisen Bank (the leading bank of the union), Banka OTP Albania, Banka Intesa Sanpaolo Albania and Tirana Bank will disburse a loan in the amount of 110 million euros in favor of the concessionaire company of the energy sector. The purpose of the loan will be to refinance an existing loan that the company in question received from the Turkish bank Türkiye ?? Bankasi (?? Bank).

Bank Intesa Sanpaolo has also decided to finance alone a loan of 26 million euros for the BALFIN group, in order to build the Mgallery Hotel in Palasa. However, the project will also be supported by the European Bank for Reconstruction and Development, which has undertaken to share the risk with the lending bank, up to 50% of the investment amount.

Last year, the American Investment Bank, Tirana Bank and Union Bank approved a joint credit line with Dragobia Energy, owned by Gener 2, the contractor for the construction of the Thumanë-Kashar road. The loan initially had a value of 26 million euros, while in March of this year, the parties signed an additional 4 million euros in the loan contract.

Dragobia Energy will use the loan funds as a debt to its shareholder, in order to finance the works for the construction of the Thumanë-Kashar road.

In 2021, Intesa Sanpaolo Bank Albania, OTP Albania and Tirana Bank financed the concession company "Orikum-Llogora" with a joint loan of 26 million euros.

Even in the case where the loans are used to finance Public-Private Partnership (PPP) projects, the Albanian government does not offer sovereign guarantees, so the banks must assume the risk of the loan themselves.

Business loans, and in particular large exposures in the corporate segment, had the main impact on the non-performing loan crisis, which culminated in 2015. Also for this reason, in the last decade, banks have tried to gradually reduce large exposures, focus on increasing lending in the retail segment.

However, in the last two years there has been a growing trend to take on large value exposures to corporate clients.

So far, the ratio of non-performing loans appears stable. According to data from the Bank of Albania, in July, this indicator fell very slightly to 4.72%, almost at the same level as at the end of 2023, but still down compared to the 5.28% level of the previous year.

However, the fact that the ratio of non-performing loans is stable, despite the rapid growth of the loan portfolio, is an indication that the amount of non-performing loans is increasing in absolute terms.

At the end of July, the total loan portfolio for the economy reached the value of ALL 798.3 billion, with an annual increase of 13.3%.

Above this value, the total amount of non-performing loans is estimated at approximately 37.7 billion ALL, from around 35 billion ALL at the end of 2023.

The NPL ratio currently remains near the lowest levels since 2008.

The further non-decline of the ratio of non-performing loans, despite the rapid increase in the size of the portfolio, may be a signal that dictates the need for increased caution in lending.

Since last year, the problem loans report has given upward signals in the credit segment for the purchase of real estate by individuals.

According to data from the Bank of Albania, the ratio of non-performing loans for this product at the end of 2023 increased to 3.2%, from about 2% in the middle of the year and 2.3% a year ago.

The loan for the purchase of real estate, mainly housing, by individuals still remains among the products with the best quality performance for the banking sector.

However, the increase in the ratio of non-performing loans can be a warning signal, given the rather high lending rates in this market segment over the past few years.

At the end of June, the Bank of Albania decided to apply for the first time a countercyclical addition to the capital adequacy ratio of the banking sector.

According to the decision of the Governor, Gent Sejko, the rate of countercyclical capital addition (KUNC) for Albania will be 0.25 percentage points, from zero that was foreseen in the previous decision. All commercial banks in Albania must complete this supplement after one year, starting on June 30, 2025.

The application of a countercyclical capital supplement is provided for in the 2018 regulation "On macroprudential capital supplements. Such an addition is aimed at slowing down lending, in case the central bank estimates that it is growing at too fast a pace.

The primary indicator in the assessment of the Bank of Albania regarding the rates of lending to the economy and decision-making on the possible need for counter-cyclical capital additions is the ratio between credit growth and economic growth.

The above ratio shows the deviation of the value of the ratio of credit for the economy to GDP from its long-term trend and is the main indicator that signals the possibility of excessive growth of credit in relation to the National Product.

This threshold would be exceeded if the deviation of the credit-to-GDP ratio from the long-term average was positive by more than 2.1 percentage points.

According to the reasoning of the Governor's decision, the values ??of the primary indicator have continued to be negative until the first quarter of 2024, but the magnitude of the negative value has decreased.

The gap in the ratio of credit to Gross Domestic Product (GDP) was -7.2 percentage points, from -7.84 percentage points that had been in the previous quarter.

But, as a complement to this primary indicator in the decision-making of the Bank of Albania, some other elements, grouped under the early warning indicator (TPHP) and which signal developments in lending and non-financial assets, specifically the real estate market, serve.

The Bank of Albania notes that, for several quarters, the Albanian economy is experiencing a positive financial cycle based on the accelerated growth of bank credit.

If we analyze the performance of credit given to businesses, for development and investment in real estate (residential and commercial), corrected for the effect of the exchange rate, the rates

annual growth rates until March 2024, have been over 30% in each case.

Further, if the loans granted to individuals and businesses are aggregated, for real estate (residential and commercial), the annual growth rate of this portfolio is 25% (from 21% according to reporting in nominal value).

This growth rate is significantly higher than the annual growth rate for the entire loan portfolio of 10% (7% according to reporting in nominal value), evidencing the acceleration of lending.

According to the Bank of Albania, such periods are associated with good levels of financial performance for the agents of the real economy and for the financial system.

"However, these periods are also associated with the beginning of certain risks, which may be related to a drop in credit standards, increased levels of its concentration in certain sectors or markets, increased debt levels for agents of the real economy beyond healthy levels etc.

These situations, if allowed to develop, can make the economy and the financial system more susceptible to various shocks, thus undermining financial stability.

For these reasons, in these cases it is suggested to use macroprudential instruments that soften the course of the financial cycle (act countercyclically) and prevent the uncontrolled development of these risks.

In our case, positive developments in the financial cycle are better reflected by the performance of the values ??of the Supplementary Early Warning Indicator (TPHP). Based on the values ??of this index during several quarters, the use of KUNC is suggested by the methodology 'For the determination of the countercyclical capital addition'", - it is stated in the argument of the decision of the Bank of Albania.

Further, the central bank adds that, if lending rates will remain high, further increases in the countercyclical surcharge rate can be expected in the coming periods.

At the beginning of this year, it was the International Monetary Fund (IMF) that suggested to the Bank of Albania the establishment of a countercyclical capital increase for the banking sector. In the statement of the IMF Executive Board for Albania, it was said that the imposition of a countercyclical addition to the capital adequacy ratio for commercial banks could be considered in the medium term, to further strengthen financial stability.

The suggestions for the application of a countercyclical rate by the IMF seem to be based precisely on the early warning indicators and mainly on the developments in the real estate market and the credit given by the banks to finance their purchase.

After the financial crisis that started in 2008, the regulators of the banking markets started a campaign of tightening the regulatory requirements, with the aim that other possible crises in the future would find the banking sector more solid and better prepared.

The Bank of Albania was quick to adopt the new regulatory requirements that were imposed in the European Union, mainly related to the new macroprudential capital additions and the framework of extraordinary intervention in banks.

This has caused minimum capital adequacy requirements to increase significantly, making banks today in theory better able to withstand shocks and potential losses from deteriorating asset quality.

In 2019, the regulation on macroprudential supplements was approved, which are added to the basic regulatory requirements of bank capitalization, which are defined in the regulation "On capital adequacy". From 12%, which is the minimum basic limit of capital adequacy, with the conservative addition of 2.5%, this limit has reached 14.5%.

With the approval of the new countercyclical supplement, the minimum level of the capital adequacy ratio next year will reach 14.75%.

Meanwhile, the capitalization requirements are even higher for a special group of banks, classified as systemically important - Banka Kombëtare Tregtare (BKT), Banka Credins, Banka Raiffeisen and Banka OTP Albania.

Currently, BKT has an additional capital adequacy ratio requirement of 1.5%, which together with the conservation allowance of 2.5% brings the total capital adequacy ratio to 16%, Credins and Raiffeisen are obliged to complete a capital adequacy ratio of capital 1% higher than other banks (in total 15.5%), while OTP 0.5% more than other banks (in total 15%).

Also, systemically important banks, as well as Banca Intesa Sanpaolo, as of January 1, 2024, must also complete the first required supplement of the capital adequacy ratio related to the minimum requirement for regulatory capital instruments and accepted liabilities (MREL).

These banks must meet an additional 1.5% in the overall capital adequacy ratio. To meet the new requirements, some of these banks will use borrowing instruments that are recognized as part of the regulatory capital.

Data from the Bank of Albania show that the average indicator of capital adequacy for the banking sector in the middle of 2024 reached 19.3%, from 19% that had been in the same period a year ago.

A factor that explains the increase in the supply of credit and the appetite for risk from the banking system is also the increase in the financial performance of the sector in recent years.

According to data published by the Albanian Association of Banks, last year, the combined profit of commercial banks with International Financial Reporting Standards (IFRS) reached 27.9 billion ALL, the highest ever recorded. System profit increased by 17% compared to 2022.

Return on equity increased to 22.17%, from 14.23% a year ago.

The increase in the profits of the banking sector came mainly from the increase in interest rates in foreign currency and from the decrease in expenses for provisions, thanks to the further decrease in the ratio of non-performing loans.

The profits of the banking sector are continuing to grow this year as well. The preliminary data of the 6 months, always according to IFRS standards, show a net profit in the amount of 19.3 billion lek, increasing by 31% compared to the first 6 months of last year.

The average return on capital at the sector level has reached 20.38%, from 16.89% in the middle of last year.

Profits have made the main contribution to the growth of share capital and capital adequacy indicators in recent years./ Monitor.al

Recently, for the second time this year, the European ...

Today, on September 22, 2024, in the foreign exchange ...

The government issued for consultation the draft for t...

In 2024, 24.5% of enterprises have sold products/services ...

Today, on September 21, 2024, in the foreign exchange ...

From September 1, the salary increase for mayors, vice-may...

Today, on September 20, 2024, in the foreign exchange mark...

The state budget collected ALL 463.8 billion until the mon...

Today, on September 19, 2024, in the foreign exchange mark...

Today, on September 18, 2024, in the foreign exchange mark...

Today, on September 17, 2024, in the foreign exchange mark...

The loan for the rehabilitation of the Durrës - Rrogozhin ...

From October 1 of this year, there will be an increase...

Today, September 16, 2024, in the foreign exchange market,...

Restrictions on the labor market for high-level profes...

The acceleration of wage growth rates in the last year...

Interest rate cut expectations have pushed the 12-mont...

The announced change of the pension scheme will be precede...

Today, on September 13, 2024, in the foreign exchange ...

The current account deficit narrowed for the second qu...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

A road accident occurred this evening on Nikolla Zoraqi St...

Three people were shot and wounded in Elbasan last night b...

A serious incident occurred this Tuesday in the Yrshek are...

An accident occurred this Tuesday on "Dituria" street in K...

All of Southern Europe will face changing weather conditio...

Albania was hit by temperatures significantly higher than ...

For the first time, Pogradec welcomed the Inter-Lake Chess...

Albania has achieved a record for the employment of foreig...

US Secretary of State Marco Rubio arrived in Manila on Jul...

In the space of a few days, Ukrainian President Volodymyr ...

The spokesman for the Iranian Foreign Ministry warned Bulg...

Autoritetet italiane sekuestruan pako me afër 800 kilogram...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

Construction company licenses will have a validity period ...

The Centralized Purchasing Operator recently opened a tend...

The new draft law "On the Bank of Albania" provides that t...

This Tuesday, one US dollar is bought for 81.2 lek and sol...