The biggest "victims" of inflation/ The pension is reduced to 25% of the average monthly salary

Retirees' financial conditions were further worsened t...

Projections show that by 2030, the working-age population will shrink systematically, while the number of pensioners will increase rapidly, putting the sustainability of the pension scheme at risk.

The development of the pension system and the increase of its financial stability is a necessity related to three main issues that require solutions.

First, the current deficit of the pension system is high, it reaches 2.24% of GDP and, under these conditions, actuarial forecasts assume a worsening of this situation.

Second, the failure of self-capitalizing private pension schemes for a period of 10-15 years in Albania has significantly reduced the replacement rate (average pension/average salary), or more precisely the average income of a pensioner.

Thirdly, the problems of unemployment, informality and especially immigration of working age have significantly reduced the percentage of the contributing population in the last 15 years, creating great social concern for the future, said Naim Hasa, Advisor of the SIGAL Pension Fund . In an interview for "Monitor", he analyzes the challenges faced by the pension system in our country and possible solutions.

How are demographic developments affecting public pension systems in our country?

Today, the problems of pensions and especially the financial deficits of the PAYGO state schemes, are a visible concern in all the countries of the world, this, among other things, also as a result of the rates with which the third population grows;

First, to increase the life expectancy of the population

Secondly, the decline in birth rates for Albania as well

Third, mass immigration

Analyzing this process, in Albania it is found that the main indicators of the operation of this system are quite worrying.

1. The rather low level of income in relation to GDP (6.88% against 10-12% of the countries around us);

2. Low contributor/beneficiary ratio 1.15 to 1, against 2 to 1 for the scheme to work well;

3. Very low replacement rate. (Average pension / average salary) 38-40%, against 70-75% legal requirements, as well as;

4. The low percentage of the population of working age included in the system (only 30-32%) etc...

Under these conditions, it must be recognized that the system generally offers low benefits with relatively high contribution loads.

As a result of all these phenomena, the development of the pension system and the increase of its financial stability is a necessity related to three main issues that require solutions.

First – The current deficit of the pension system is high, it reaches 2.24% of GDP and, under these conditions, actuarial forecasts assume a worsening of this situation.

Second - The failure of self-capitalizing private pension schemes for a period of 10-15 years in Albania has significantly reduced the replacement rate (average pension/average salary), or more precisely the average income of a pensioner.

Third - The problems of unemployment, informality and especially immigration in working age have significantly reduced the percentage of the contributing population in the last 15 years, creating great social concern for the future.

Projections show that by 2030, the working-age population will shrink systematically and, on the other hand, the number of pensioners will increase rapidly, putting the sustainability of the pension scheme at risk. Thus:

The age group over 60 today occupies 23.5% of the total population at a time when this population in 2001 was only 11%;

The birth boom of the 1960s is bringing a rapid rise in retirees this decade, as the working-age population is shrinking rapidly from declining births and high immigration.

A problem that requires a solution is the financing of pension schemes in rural areas.

Currently, only 10% of farmers, about 60,000 people, pay contributions, causing about 80% of pension expenses in rural areas to deepen the deficit of the scheme. As the social insurance scheme works today in rural areas, it is not just an insurance scheme.

Required:

a) The law should be binding on all able-bodied farmers, or

b) Return to a voluntary insurance scheme, as is done today in many countries of the world.

Are private pension funds a good option to secure higher retirement income and why?

Analyzing the pension system in Albania in its entirety, especially its functioning, it must be accepted that self-capitalizing pension systems are today presented as a necessity of the time.

As is known, the PAYGO solidarity scheme is thought to have fulfilled its mission well, they were very effective when we had a young population, where many worked and contributed and few benefited - pay less and get more.

But in the conditions of population aging, where these ratios have changed, now - pay more and get less and less, almost all over the world, for developed countries after 1980 and for developing countries after 2000 have entered as components of a pension and private self-capitalization schemes.

These are also the reasons that today private (self-capitalized) pensions are developing at high rates in all countries of the world.

The gradual aging of the population and emigration, which has mainly included young people in Albania, is significantly changing the structure of the population in the country, inverting the pyramid in favor of the third ages.

For Albania's conditions, we think that the introduction of the private self-capitalizing system of pensions is more suitable and functional, according to:

First, in Albania, approximately 75-80% of GDP comes from the private sector, so there is no reason not to evaluate it in this area as well.

Secondly, Albania is a European country and the harmonization of legislation in the field of social security is a condition for joining this family.

Thirdly, these schemes, by their very configuration, better help the country's economy, mobilizing the free money of the population through their investments in long-term financial instruments of 5-10-15 years (State Bonds), which returned to the participants in these schemes in two forms as investments in social life, infrastructure, education, health and as a safe and guaranteed net profit in members' assets.

Fourthly, the development of the private self-capitalizing pensions market will give a very positive impulse to other actors operating in the financial market.

I think the situation is known, there is no need to comment, what matters is what we will do.

Among the measures that must be taken to improve the pension market, we can say with complete conviction that it is the development of private self-capitalizing pension schemes. Rightfully so, today this system is considered a necessary requirement of the time.

Albanian legislation currently allows the operation of two systems (columns). The state system and the supplementary voluntary private system. To increase the replacement rate (the ratio between the average salary and the average pension), which is currently 40-44%, against the 70-75% it should be, private schemes are required to be developed.

First, promote the newly created voluntary supplementary pension scheme. According to the law, this scheme performs two functions,

a) provides additional pensions above those provided by the mandatory state system and

b) grants pensions under more favorable conditions than those offered by the basic scheme.

This scheme needs greater care, through the fiscal system, fiscal facilities, expanding the types of funds, especially professional ones, for difficult professions, etc.

In order to increase the interest in participation, the initiative of the Financial Supervision Authority and the Pension Market to improve the legal framework should be appreciated, but let's not forget that it is partial and it is required to work harder for the full completion of the legal framework in this field.

Secondly, to establish the forced private system, which will require a division of the contribution into two parts, a social contribution that will have to cover the current pension system and an individual contribution part, which will flow into the fund's own accounts of pensions.

With the establishment of these schemes, the possibility is created for the operation of the multi-column system of social security in Albania as well.

Are changes needed in the pension reform carried out in 2014? If so, what interventions should be made?

Of course, I appreciate the reform that was undertaken in 2014 for the social security system in general and the pension system in particular, which, through the parametric reforms it contained, aimed to:

First, to stop the further deterioration and deepening of the financial deficit that in the last 10 years was affecting the pension system, gradually increasing the retirement age of women and their comparison with men and increasing the length of seniority in work to get a full old-age pension.

Second, to establish a social pension for the third age who do not have conditions for work pension.

Third, to establish precise and clear pension indexation rules, based on the increase in the price index, etc.

But we must admit that this reform was partial. A stable solution and a long-term reform would be the establishment of the mandatory private self-capitalization system, the second column, as an integral part of the general pension system, as all countries have, even those around us such as; Croatia, Bulgaria, North Macedonia, Kosovo, etc.

These situations that the pension system in Albania is going through have laid the need for its reformation, focusing on finding suitable and fair financing ways, creating a shared responsibility of covering vital needs in old age, between the state and the individual. .

One of the systems that is being successfully installed and developed today in Europe and beyond is the establishment of the Alternate Pension system, with two important components, a consolidated basic public system and a developed private system, mandatory for the new generation. and voluntary for all those who want a higher pension.

This system presupposes a division of the contribution into two parts, social contribution for the state PAYG scheme and individual contribution for the private self-capitalization scheme. While the voluntary scheme is left free, those who want more become participants in these schemes.

This model, in addition to all developed countries such as Germany, France, Italy, etc., is also found in Poland, Hungary, Croatia, Bulgaria, Estonia, Romania, Czech Republic, Slovakia, Kosovo, North Macedonia, etc., which according to concrete conditions have made the division of contributions and dynamically follow the evolution of these processes. Only three countries of the Western Balkans, Albania, Bosnia and Serbia, have not completed the pension system with the second private column, which is also the reason that the level of pensions in these countries is very low.

By establishing an alternating pension system with two important components, a consolidated basic public system and a developed private system, premises are created, not only in the gradual improvement of the financial situation of the pension system, but also the country's economy is helped, mobilize the savings of the population through contributions to investments in their economy.

Private pension systems provide solutions to many problems dictated by time:

first, they solve the generational conflict, making the new generation more interested in insurance;

secondly, they solve the problems of the distortion of the labor market, quite disturbing for the Albanian economy, which accounts for about 32% of informality, both in the case of black and gray evasion, since the contribution measure is very well related to that of benefit.

Thirdly, they offer benefits under more favorable conditions of age, length of service and pension measure. And they have a very favorable transparency and fiscal system.

These are also the reasons that today private (self-capitalized) pensions are developing at high rates in all countries of the world.

The establishment of the mandatory private pension system by allocating 3-5% of the contribution to self-capitalization schemes is also conditioned by the Albanian state's need for financial resources. Through the establishment of the self-capitalization scheme, investments in the economy increase, mobilizing the insured's assets that are invested in long-term state bonds.

From the figures published by the Institute of Social Insurance, according to some estimates, 13.5 billion ALL, or 96.5 million euros, are accumulated in these schemes for a year, which increase every year progressively and only after 10 years, they reach 230-250 billion ALL. or 1.750 million euros.

The possibility of their mobilization for the country's economy would require that it be specified in the law, like many developing countries, that the first 10 years be invested only in financial instruments within the country.

Private pension funds are such an urgent necessity that they cannot wait for the local capital market environment to develop to start their activity, on the contrary, as in many developing European countries, they will be the very ones that will condition the creation and the development of this market.

Experts in the field, including you, have often requested legal changes in order for the voluntary pension market to grow in Albania and be competitive. Does this law that was approved during the fund meet your requirements? How does it help the market?

It has already been accepted that the activity of private pensions in Albania has developed in an environment where the necessary infrastructure such as the capital market, full fiscal incentives, especially for employer beneficiaries, dysfunctional legal framework suitable for the time, etc. have been missing. In this context, I highly appreciate the approved law and the improvements it contains, which aim to bring new development to this market and concretely.

First, they make the legislation that regulates these relations more acceptable for the time, reflecting also the problems that arose during its practical implementation, in this period of nearly 10-12 years of their activity;

Second, it makes the parties participating in a Voluntary Pension Fund both contributors and beneficiaries more interested, through a more favorable fiscal system.

I think that the tax treatment of voluntary private pensions is an important policy choice in the pension reform that is being undertaken. A fair tax treatment encourages membership in individual schemes, or professional schemes in the case of companies.

These changes that were approved solve the non-taxation of the contributions of both individuals and employees, as well as employers up to an acceptable level for the time, which is linked to the minimum wage, and every time it changes, the tax-free limit also changes automatically. .

Also of particular importance are the application of tax benefits and at the time of benefits, harmonizing with other legislations issued in the field of pensions.

Thirdly, from a structural point of view, the improvements make the law more complete and up-to-date with international provisions, recommendations in the field of voluntary private pensions by international organizations.

The law provides for the operation of two forms of pension funds: "Pension fund with open participation", which does not provide for restrictions on membership, and "Pension fund with closed participation", where participation in this fund is limited only to employees or members of entities that create a closed fund, creating administration spaces and other laws issued in the field of pensions, such as those of difficult professions.

Fourthly, the law foresees a decrease in the annual commission of the Fund's asset administration to 2.5%, from the previous 3%, leaving more opportunities for the fund's members to participate in the profit.

Fifth, I think that this law will also apply to the laws that have been and will be issued in the future for professional pensions for difficult professions, such as No. 29/2019.

I am convinced that these improvements provided for by the approved law will enable the development of the private pension market and, more broadly, the capital market, and consequently will facilitate the public scheme, which is mainly (45%) financed by the state budget and that that, more and more as a result of demographic processes, let state social schemes be compensated by private self-capitalizing schemes, ensuring a higher and stable income coverage for the participating individuals, improving the economic and social development of this layer of society./ Monitor magazine

Retirees' financial conditions were further worsened t...

Today, on November 11, 2023, the US dollar is bought a...

The former president of the European Central Bank, Mario D...

Today, on November 10, 2023, the US dollar is bought at 97...

Liabilities to the public distribution company reached...

Today, on November 9, 2023, the US dollar is bought at 97....

The reform of the pension scheme is under revision in ...

Today, on November 7, 2023, the US dollar is bought at 97....

The capacity utilization rate is increasing for the se...

Many families in Kosovo are being forced to go into de...

Allocate 2.2 billion lek in the 2024 draft budget to the f...

Ndonëse vendi ka shënuar rritje të kënaqshme vitet e fundi...

Today, on November 7, 2023, the US dollar is bought at 97....

The draft budget 2024 sets a new level regarding the plann...

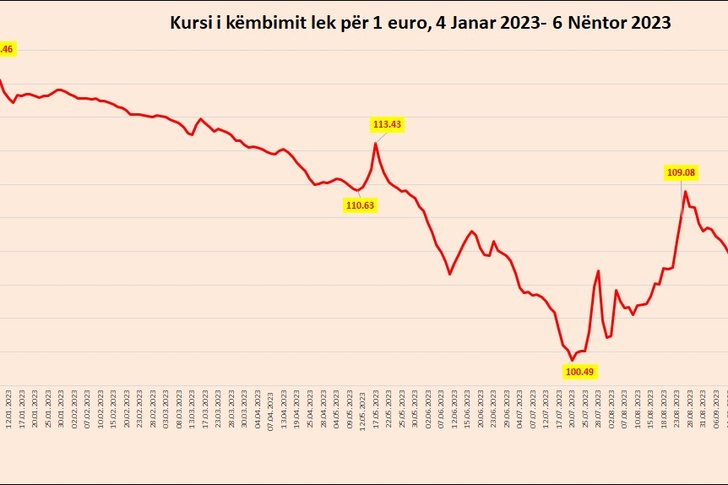

The lek has started the week with further strengthening in...

After the construction boom of the last two years, the sec...

Today, November 6, 2023, the US dollar is bought at 97.5 A...

The production of olives this year marks a decrease in Alb...

Albania has reached the highest peak this year, in the con...

Today, November 4, 2023, the US dollar is bought at 97.4 A...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

Footage emerges from the serious accident that occurred th...

A Shkodra traffic police officer was hit with hard objects...

This Wednesday, around 4:00 PM, a serious accident occurre...

Tirana Police have shared details regarding the accident t...

A serious accident that occurred this Wednesday with the c...

The Institute of Geosciences has shared a forecast for wea...

Rising energy and fertilizer prices are expected to contin...

Over 18,000 foreign citizens from 140 countries have appli...

The trial of ousted Venezuelan President Nicolas Maduro on...

US President Donald Trump has issued another warning to Ir...

Prime Minister Andy Burnham has announced that most bus fa...

France's parliament has passed a law to ban social media f...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

The price of diesel reached 206 lek per liter from 198 lek...

Businesses will no longer be required to simply register t...

Despite economic growth and income in recent years, Albani...

This Wednesday, one US dollar is bought for 81.4 lek and s...