Euro at the rate of 103 ALL/ Exchange rate, December 17, 2023

Today, December 17, 2023, the US dollar is bought at 94.4 ...

Debts, the mountain of debts, the burden of debts - in many German media there is a notion that has been worn by Germany for a long time, "German fear", the German fear of very large debts.

The outside world looks more coldly at this issue. Germany has many problems, but debts are not the problem, writes the well-known magazine "Economist", in the face of the German debt dilemma, after the decision of the Constitutional Court to declare invalid the reorientation for other purposes of 60 billion euros of loans reserved by the pandemic . Now this money is missing for important investments. So save or take on new debts?

When are debts dangerous? The simplest answer would be: always when it becomes too expensive for the states to pay. And dangerous they become when Christian Esters and his team put their thumbs down. Esters heads the agency S&P for the evaluation of public debts. S&P is the most powerful credit rating agency, ahead of Moody's and Fitsch. The agency's decisions can have ramifications for many countries because they determine when countries are insolvent and how much new debt costs. The worse the ratings, the more expensive it becomes to take on new debt.

The level of debts also plays a role in assessing the financial situation, Esters told DW. Here, for the S&P agency, the level of debts measured by gross domestic product is important. Germany, with a rate of 66% compared to the world, is in a relatively good position. Other countries such as the USA or Japan, measured by economic capacity, are in a worse condition in terms of the level of debts.

One measure that is always used is the total public debt. The clock of debts is known: Since 1950, its hands always move in one direction: currently the total public debt of Germany is 2.5 billion. Within the Eurozone, Germany is in third place after France and Italy. But for Esters from the S&P agency, the total debt of a country is not a very important indicator. "The debt of a state absolutely ignores the relationship with the popular economy," says the expert. Sometimes debt per capita is taken as another measure. In Germany, this debt is 31,000 euros per head.

But this measure does not play a big role in the creditworthiness of a country. Because especially the countries of the global north, according to this assessment, are more deeply in debt than the expanding countries with large populations. Even Esters does not see such a measure as relevant. Comparing rich countries with poor ones makes no sense and is misleading, he says.

Government debt is only one aspect in assessing creditworthiness. "There are a number of other factors, such as interest rate costs on public debt." The higher the interest rates, the more expensive the debts become. And how high interest rates are depends on inflation. If inflation is high, central banks try to counter with high interest rates - if they have an effect. According to Esters, "inflation is one of the factors that co-determines the effectiveness and reliability of monetary policy".

In terms of inflation, Germany is at an average level compared to the world. World inflation in recent years has increased, but compared to the 80s or 90s it is moderate. "High inflation can lead to the weakening of purchasing power and the decline of competitiveness in the world," says Esters. Therefore, inflation is an important measure for rating agencies.

There are also political factors. "It is important to emphasize that we do not consider only fiscal factors. Especially the last few years have shown that the predictability and stability of institutions play an important role. States can fall into a debt crisis also because of weak institutions in the country". But here the circle closes, because debts can play an important role. Thus, S&P has concluded that the world public debt has increased by 8%. This in turn increases the pressure on the state budget, especially when interest rates are high. "A large portion of state revenue must be given to pay interest rates. This limits fiscal flexibility, for example to react to future shocks or crises."

That high debts do not necessarily have to do with lower reserves of household economies, this is shown by the savings quotas in Germany and the USA. Despite the high debts in the past years for the Corona packages, the restructuring of the economy and the war in Ukraine, S&P has had more positive credit ratings. As for the coming years, Esters has a different attitude. "We expect in one or two years more negative evaluations than positive ones." Decisive for development are not mountains of debt, but political risks. Even for Germany, the expert Esters is optimistic, despite the new debts./ DW

Today, December 17, 2023, the US dollar is bought at 94.4 ...

The progress of the indicators that are monitored with...

Today, December 16, 2023, the US dollar is bought at 93.8 ...

The project for the transformation of the entrance of ...

Since the Territorial Reform of 2015, the local government...

Today, December 15, 2023, the US dollar is bought at 9...

Tabelat e buxhetit faktik të vitit 2022, të cilat janë mir...

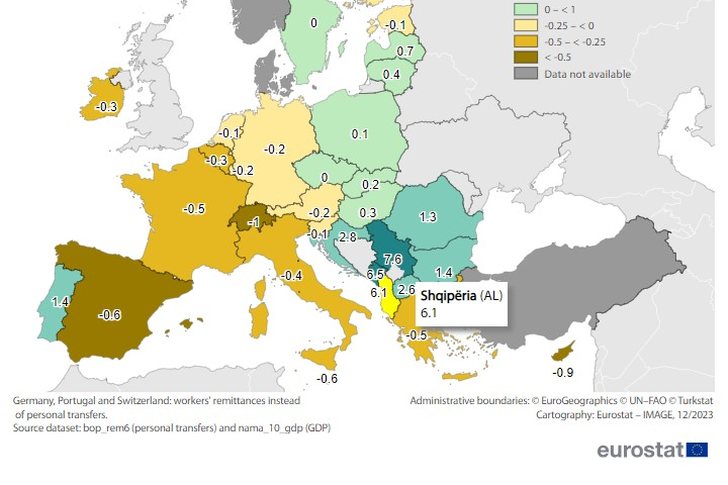

Eurostat data show that the value of remittances that ...

The affair of the incinerators with 178 million euros ...

Eurostat data show that the value of remittances that ente...

Economic activity in our country peaked in the third quart...

Today, December 13, 2023, the US dollar is bought at 9...

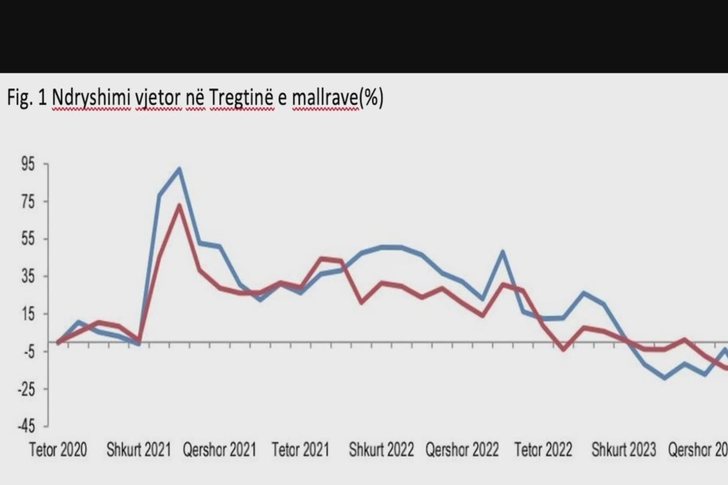

For the first time in its history as an open economy, ...

The official unemployment rate in Albania reached 10.5...

Sot më 12 dhjetor 2023, dollari amerikan blihet me 94 ...

In November last year, the average inflation in the Eu...

Komisioni Europian (KE) ka paralajmëruar në raportin e...

Today, December 11, 2023, the US dollar is bought at 93.9 ...

The chairman of the association of exporters of Albania, E...

Sot më 10 dhjetor 2023, dollari amerikan blihet me 94 ...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

This Wednesday, around 4:00 PM, a serious accident occurre...

Tirana Police have shared details regarding the accident t...

New details have emerged regarding the accident that occur...

New details have emerged from the serious accident that oc...

A serious accident that occurred this Wednesday with the c...

The Institute of Geosciences has shared a forecast for wea...

Rising energy and fertilizer prices are expected to contin...

Over 18,000 foreign citizens from 140 countries have appli...

The trial of ousted Venezuelan President Nicolas Maduro on...

US President Donald Trump has issued another warning to Ir...

Prime Minister Andy Burnham has announced that most bus fa...

France's parliament has passed a law to ban social media f...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

The price of diesel reached 206 lek per liter from 198 lek...

Businesses will no longer be required to simply register t...

Despite economic growth and income in recent years, Albani...

This Wednesday, one US dollar is bought for 81.4 lek and s...