The car ends up in the canal/ The driver is injured in Gramsh

An accident happened this Sunday evening in Gramsh, where ...

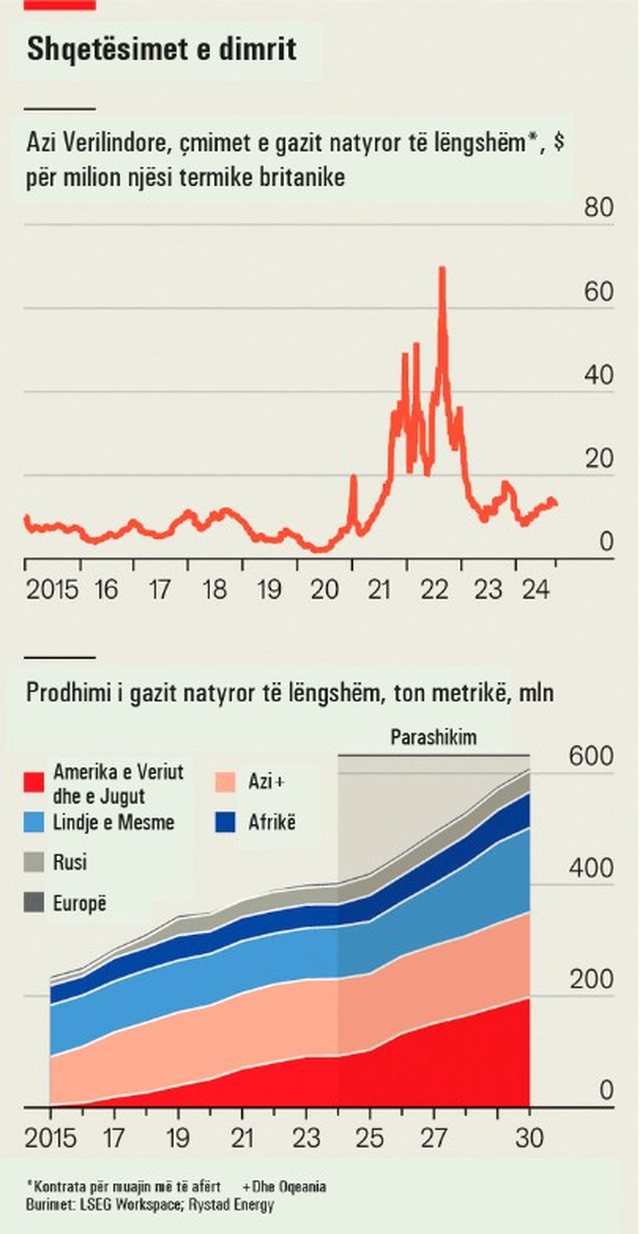

A po shkon bota symbyllur drejt një krize tjetër gazi? Çmimet mund të rriten sërish këtë dimër

Gastech, a gas company in Houston, was very optimistic. After a series of agreements from energy ministers and fossil fuel giants, delegates cheered: it was decided that their product would play a key role in the green transition.

However, there was also uncertainty. President Joe Biden has suspended permits for US liquefied natural gas export terminals.

There are also concerns that the global market for liquefied natural gas, which became vital to Europe and Asia after the start of the war in Ukraine, may soon face its first real test. With demand increasing and supply failing to come into circulation, a new scramble for gas could begin.

During the worst energy crisis, it looked like 2025 would be the year of salvation. Russia had shut down pipelines supplying more than 40% of European gas.

As the European continent began to try to survive the next two winters and get out of the trouble caused by dependence on Russia, large projects in America and Qatar for liquefied natural gas flooded the European market.

In fact, Europe not only survived the energy crisis, but also exceeded its own expectations.

The third winter since the war in Ukraine is approaching and gas storage capacities are fully 94% full, surpassing the goal of filling them to 90% by November. Purchases of large quantities of liquefied natural gas, which last year accounted for 60% of gas imports, have helped here.

However, the market is worried. Asian liquefied natural gas prices, a global benchmark, are above $13 per million British thermal units (mBtu), higher than at almost any time except for the 2022 panic period.

One concern is the rapid drop in temperatures. The past two Northern Hemisphere winters have been mild, but the upcoming winter is unlikely to be as mild.

"Even a normal winter would feel very cold by the standards the last two winter seasons have created," notes one gas trader. A cold season would be doubly bad for Europe. It would require more gas, not only for heating, but also for electricity: cold weather tends to come with a weak wind, reducing the output of wind farms.

Northeast Asia will also experience a colder winter than in recent years. An extreme winter season like that of 2021 is also possible, when Beijing endured temperatures down to -20°C in January, the coldest winter in 50 years.

Sindre Knutsson, from consulting firm Rystad Energy, calculates that a major cooling in Europe and Asia would create additional gas demand of 21 billion cubic meters (bcm) and 15 bcm respectively.

As Europe is maximizing pipeline imports and Asia with the exception of China has negligible pipeline trade, the remainder would have to come from seaborne shipments. This could create an additional demand for liquefied natural gas of 26 million tonnes, equivalent to 7% of volumes traded globally last year.

The second concern is that Europe's pipeline imports could fall. Under a five-year deal that expires in December, Russia still sends gas through Ukraine to central Europe. These flows have been halved since 2021, but still amounted to 15 bcm last year. Ukraine has already said it will not negotiate a new deal.

Europe and Ukraine are talking to find a solution. More realistic would be an "exchange" with Azerbaijan, where Russian gas coming through Ukraine would be relabeled as Azerbaijani gas, while a part of Azerbaijan's gas would become Russian.

Azerbaijan would then be free to buy that gas for itself, or send it to Turkey. However, even under this scenario, Europe would still be short of gas.

It would receive as much as before through Ukraine, but less from Azerbaijan. Moreover, because energy is cheap in Azerbaijan, Russia would have to agree to sell gas to Azerbaijan at a low price, or Azerbaijan would have to pay beyond its means.

And at any time, Russia can decide to stop deliveries of "Azerbaijani" gas to Europe. Talks have so far not progressed.

Therefore, weather and geopolitics could create demand for much more liquefied natural gas, and this could happen at a time when the market is quite turbulent. Russia's main liquefied natural gas terminal, called Arctic LNG 2, has faced delays and lost customers after America imposed sanctions on the project and fined ships that dock there.

A plan for Egypt to become a reliable supplier of liquefied natural gas to Europe has also been destroyed. Gas production in the country is declining much faster than expected.

The biggest disappointment has actually been America. Mr. Biden's moratorium will hit supply, but only after several years, as it only applies to new projects.

America's most pressing problem is the bankruptcy of the prime contractor on Texas' Golden Pass project, one of two major terminals slated to come online next year, which could cause delays of six months or more.

Along with setbacks in smaller projects, this means that of a new capacity of 25-30 mtpa expected by 2025, only 15 mtpa could materialize.

What would a perfect storm look like? The worst-case scenario would include sub-zero temperatures in Europe in early December and the disappearance of Russian gas by January 1.

However, the continent will not run out of fuel in the short term, because in addition to record reserves, it has abundant nuclear power (many French nuclear plants that were closed in 2022 have now reopened) and hydropower (after heavy rains).

But Europe's gas reserves would deplete much faster, leading to the first major test of replenishment since 2022. This time Europe's "appetite" for gas would be even greater: as it has expanded capacity of regasification by a fifth, it is less constrained in its acquisition ambitions.

Europe will have to compete with Asia for liquefied natural gas cargoes, which would lead to increased spot prices. Anne-Sophie Corbeau at Columbia University thinks these prices could easily reach $16 per BTU by the start of the year.

Richer Asian countries and China would be largely protected because they buy most of their liquefied natural gas with long-term contracts that are indexed to the price of oil.

In contrast, almost all of Europe's purchases are made either in the spot market or indexed to spot prices, and the continent cannot live without gas, having shut down most of its coal-fired power plants. Governments, utilities and consumers would have no choice but to bear the higher cost.

Poor and developing economies would suffer much more severely. Lured by lower prices from last year, some have recently returned to the market, or even imported liquefied natural gas for the first time.

Rising prices would certainly bring this development to an abrupt end. Many would be forced to switch back to coal; some may be forced to continuously cut power. The wait for new supplies can be long./ Monitor.al

An accident happened this Sunday evening in Gramsh, where ...

The former political prisoner, Beqiri, told this Sunday th...

The former deputy of the Socialist Party, Jurgis Çyrbj...

Prime Minister Edi Rama has returned to meetings with ...

The youth of FRPD gave a slap to the mayor of Tirana, Erio...

The RENEA Special Unit, based on the training program appr...

A group of young people appeared today at the Tirana M...

The Tirana Marathon is being held this Sunday. As this ev...

The entrepreneur and businessman Gjergj Luca has spoken to...

After the competition for the new director of the State Po...

The Central Election Commission has sent a request to the ...

Argita Malltezi reacted after the report by judge Irena Gj...

Judge Irena Gjoka has summoned Argita Malltezi. Gjoka has...

I believe that everyone who reads these names feels di...

The member of the Regulatory Commission in the CEC, Muharr...

Today, the meeting of the Regulatory Commission is taking ...

Prime Minister Giorgia Meloni does not back down after...

The Minister of Education and Sports, Ogerta Manastirl...

CNA has carried out an investigation on medical oxygen whe...

A court in Rome on Friday ordered the return to Italy of t...

Dritan Prençi is the SPAK prosecutor who is sleeping on th...

The in-depth investigations that SPAK conducted into Ajola...

SPAK's standards, the way it investigates, how it secures ...

Irfan Hysenbelliu claims to be a big businessman, an hones...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

In Korça, a 4-year-old child accidentally falls from the s...

A 33-year-old Albanian citizen was arrested in Italy after...

One of the perpetrators of the explosion that occurred yes...

A case of heroin trafficking from North Macedonia to Alban...

Today our country will be affected by unstable weather con...

On Thursday, our country will be affected by relatively un...

Albania is facing a deep demographic crisis where official...

This Wednesday, our country will be affected by relatively...

The global economy is expected to face its biggest slowdow...

German Chancellor Friedrich Merz (CDU) defended his govern...

US President Donald Trump has made a post on Truth Social ...

US President Donald Trump announced today that he was canc...

At the Museum of Fine Arts in Chambéry, France, an exhibit...

Korça has transformed this weekend into the capital of cel...

Korça is ready to open the summer season with one of the c...

Two years after his passing, the renowned Korçë poet Skënd...

The average rent for apartments in Tirana for 2026 has rea...

This Friday, one US dollar is bought for 81.8 lek and sold...

The price of gold fell to its lowest level in more than si...

Businesses reduced their borrowing abroad last year. Bank ...