Monedhat që pësojnë ulje/ Kursi i këmbimit, 4 maj 2024

Sot, më 4 maj 2024, në tregun valutor, dollari amerika...

Last year was expected to be delicate again for the banking sector, especially due to the possible effects of the increase in interest rates and the slowdown in economic growth. But the effects of these developments turned out to be much weaker than expected.

Deposits, credit and total assets continued to grow, while the ratio of non-performing loans fell further to a new low since 2008.

The relatively good performance of the economy in relation to the general global environment certainly played an important role, supported especially by a positive cycle in tourism, services and real estate.

The effects of rising interest rates were largely positive, increasing net interest income. The strengthening of the lek helped to maintain the solvency of borrowers and to maintain lower interest rates for the local currency, a factor that further influenced a strong increase in new credit.

A very important development of the past year was the further shift of banking services towards digital channels.

Now, the majority of bank transfers are carried out through electronic channels. In the most visible aspect, this is an indicator of the modernization of the market and the increase in speed and convenience in obtaining banking services for the public.

But digitalization is also important for cost optimization and better use of human resources, at a time when the departure of professionals has become a problem in the financial market as well.

Human resources are being used less and less for basic processes, such as collecting payments or making transfers, and more and more for more specialized services, especially related to consulting and strengthening the relationship with customers.

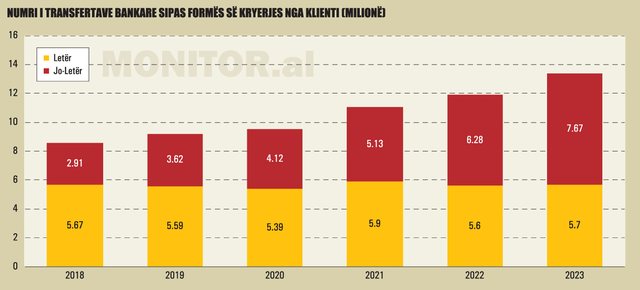

Transactions through electronic channels dominated the structure of bank transfers for the second year in a row in 2023.

According to data from the Bank of Albania, out of about 13.4 million credit transfers made by customers of the banking sector, more than 57% of them, or about 7.7 million actions in total, were made in non-paper form.

Transfers in non-paper form include transfers that are carried out without the client's physical presence in the bank, through internet banking and mobile banking services.

Compared to a year ago, customers of the banking sector increased the number of remote banking operations by 22.1%, or by 1.4 million operations more.

Their specific gravity has increased rapidly in recent years. In 2018, non-paper payments accounted for less than 34% of the total, while within five years, their weight has reached more than 57%.

The share of digital actions has also increased significantly in value. Last year, the value of bank transfers executed in non-paper form accounted for 34% of the total, from about 21% in 2018.

In 2023, physical money transactions performed by customers at bank counters declined not only in specific weight to total transactions, but also in absolute value. Cash operations in banks decreased by 2.1% in number and 0.2% in value, compared to 2022.

The use of online channels saves time and is an important development for avoiding customer queues at bank counters, using these counters only to obtain those services and products where physical presence is really necessary.

By the end of 2023, the number of bank accounts connected to the Internet reached almost 1.1 million, growing by almost 25% annually.

It is estimated that now 34% of active bank accounts are accessible from the Internet, from 28.2% that was this indicator at the end of 2022.

More than 90% of the number of resident bank accounts connected to the Internet belong to individuals. However, the largest increase in Internet-related accounts last year was in the business segment, up 25% compared to the previous year.

For any individual or entity that owns a bank account, the vast majority of payments and transfers can be made via the Internet, without the need to physically go to the bank.

The use of payments through electronic channels has also been facilitated by the Bank of Albania. Since June 2020, all interbank transfers up to the value of 20,000 lek that are carried out through electronic channels must be offered by banks without any commission.

For larger amounts, electronic transfers have commissions at least 50% cheaper compared to those carried out from bank counters.

The same policy was followed in the regulation for national transfers in euros, where commissions for electronic transfers must be a maximum of 50% of commissions for payments made in bank branches.

Currently, all commercial banks in Albania offer remote banking services. This means that every client of the banking sector has an alternative channel available for making payments and receiving other services, without necessarily going to a branch.

Digitization of banking services is one of the reasons that have led to a decrease in the number of bank branches in recent years.

The updating of the legislation on electronic identification and signature is expected to increase the number of banking services and products that can be offered remotely.

Reducing the high rate of use of physical money is a big challenge for the Albanian economy. Despite the rapid growth of electronic payments, the use of physical money in the Albanian economy remains a dominant phenomenon, which carries high costs for the economy.

According to the Bank of Albania, the ratio of money outside banks to liquid money (monetary aggregate M1) last year was again at a fairly high level, 51%, although down from the level of 52.7% of the previous year.

The high use of cash determines a higher degree of informality and fiscal evasion, which reduces the possibilities of the state budget to increase the quality of public services.

Most people, on the other hand, find it difficult to understand that the use of cash is not a cost-free payment method, but on the contrary is costly to an economy, if one considers the costs of accepting these payments, the costs of cash storage and transportation and if the operational risk associated with physical cash is quantified.

For this reason, increasing the use of digital payments not only to replace bank transactions, but also payments at the point of sale is very important for the economy.

These payments continue to have bank cards as their main instrument, although in recent years payments with alternative electronic money technologies have also begun to be used.

Last summer, the European Commission recommended to Albania the establishment of a ceiling amount for physical cash payments.

In the last report of the analysis of Albania's compliance with the EU legal and regulatory framework, the European Commission assessed that our country is only partially compliant with the European Union framework in terms of money laundering investigation.

Despite recent progress, Albania's legislation is partially aligned with that of the EU in this area.

A similar request for setting a ceiling for cash payments has been expressed for years by the Albanian Association of Banks. According to the Association of Banks, the reduction of physical money in circulation and commercial transactions is a challenge and a requirement for a more organized, more measurable, more disciplined and more stable economy.

According to the Banking Association, setting a ceiling on cash payments by individuals would help reduce tax evasion and help fight money laundering and financial crime in general.

Also, the Association of Banks has asked the government that businesses in Albania are forced to accept at least one alternative method of payment, apart from physical money.

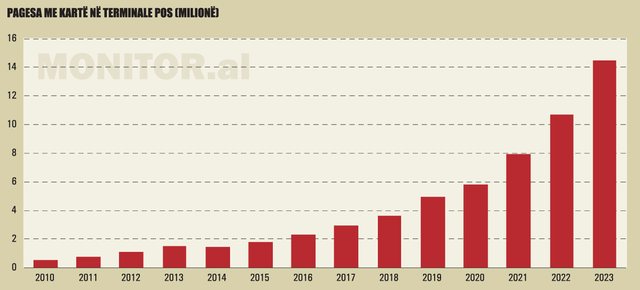

Bank card payments again registered strong growth last year and touched historical highs in number and value of transactions. According to statistics from the Bank of Albania, during 2023, card payments at POS terminals (electronic points of sale) reached almost 14.5 million, with an increase of 35% compared to the previous year.

In transaction value, card payments last year reached 64.1 billion ALL, 26.6% more compared to 2022.

For 2023, the volume of payments at POS terminals accounted for 14.5% of the total value of card transactions, from 13.9% that had been the weight of these transactions a year ago.

Card payments are being driven especially by the record growth of inbound tourism. The demand from foreign tourists to pay by card is pushing more businesses to accept payments with these instruments.

According to data from the Bank of Albania, the number of POS terminals for accepting card payments, at the end of last year, reached a record number of 19,184, an increase of 18.2% compared to the previous year.

The number of active bank cards at the end of 2023 reached 1.43 million, an increase of 4.6% compared to the previous year. The number of debit cards reached 1.24 million, an annual increase of 5%.

This product remains dominant and accounts for almost 87% of the total number of bank cards. The debit card is a basic payment instrument, linked to the current accounts of businesses and individuals.

The year 2023 was also positive in the credit card segment. At the end of last year, the banking sector reported almost 120 thousand active credit cards, with annual growth of 6.6%.

Although the development of this product in the Albanian market is still weak, the number of credit cards has reached the highest historical figure.

Last year, the two global giants Visa and Mastercard completely dominated the bank card market in Albania, while American Express completely left the market, along with other cards issued by local entities.

Bank of Albania data show that at the end of 2023, Albanian commercial banks had over 729,000 active cards issued with the Visa brand, a figure that increased by 3.8% compared to the end of 2022.

However, Visa's market share has fallen to 50.9% of the total number of active cards in Albania, from 51.3% at the end of 2022.

Mastercard, at the end of 2023, reported almost 704 thousand active cards. The number of Mastercard cards has increased by 5.4% more compared to 2022.

Cards issued with the Mastercard brand accounted for 49.1% of the total number of active cards, up from 48.7% a year ago.

American Express, last year, left the Albanian market and according to the statistics of the Bank of Albania, there were no longer any active cards issued in its name.

The exit of American Express from the market came after the merger of Alpha Banka Albania, the last commercial bank in Albania that still issued cards of this company. In December 2022, Alpha Bank Albania legally merged with OTP Bank Albania.

Even local cards, which had been in negligible numbers anyway, have completely left the market last year.

The high use of cash in the economy is a reality that will still take time to change. However, even in cash transactions, technology offers automation opportunities, so that depositing money in banks is done at a lower cost and in a faster time.

Deposits of money at ATMs increased for the sixth year in a row in 2023. According to Bank of Albania statistics, for 2023 banking sector customers made more than 769 thousand automatic deposits at ATMs, an increase of 34% compared to the previous year seen. Since 2020, cash deposit actions at ATMs have increased by four times.

The increase in transactions is also significant in terms of value. For 2023, cash deposits at ATMs were worth 37.9 billion lek, an increase of 27% compared to the previous year. Even the value of ATM cash deposits has increased more than four times since 2020.

The growth is also supported by the continuous expansion of the equipment infrastructure that enables this type of service.

The number of ATMs with the function of depositing physical money is increasing, a fact that proves the increasing investments of the banking sector to automate the provision of banking services.

Data from the Bank of Albania show that the number of ATM devices enabling cash deposits at the end of 2023 reached 370, with an increase of 21% compared to 2022. Approximately 40% of the total number of ATMs in the country offer a cash deposit service.

The addition of ATMs with the function of depositing money is an important development for facilitating the provision of banking services. Albania remains an economy with a high use of cash in economic transactions.

This creates the need for periodic cash deposits in bank accounts, and transactions with cash in the cash register remain one of the main reasons for the flow of customers to bank branches.

The automation of this service through ATMs affects the reduction of flows, the reduction of queues and the use of bank branches only for those cases where the provision of the service by the staff is necessary.

At the end of September, the Albanian banking sector offered service through 925 active ATMs, an increase of 8% compared to a year ago. The number of ATMs had continuously decreased in the period 2015-2019, especially due to the decrease in the number of branches, but also due to the decrease in the total number of commercial banks.

But, starting from 2020, even under the impetus of the pandemic, banks increased the number of ATMs (mainly located in environments outside branches), in order to facilitate the flow of operations at the counters.

At the same time, the addition of ATMs is being accompanied by updating the technology and the services offered by them.

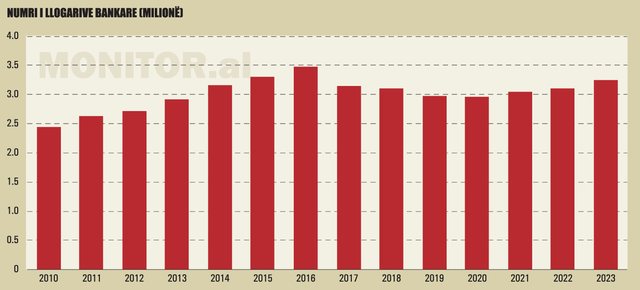

The number of accounts in the banking sector increased for the third consecutive year in 2023. Bank of Albania data show that the total number of bank accounts at the end of last year reached 3.24 million, with an increase of 4.2% compared to the previous year.

Over the past year, the number of active accounts in the banking sector has expanded by approximately 127,000.

The number of bank accounts in Albania reached the highest number in 2016, with almost 3.5 million. In the period 2016-2020, their number suffered a continuous decrease, especially due to the decrease in the number of banks, as a result of the consolidation process of the sector. However, after 2021, a new upward trend is being noted.

The number of bank accounts of resident subjects in Albania increased last year in the individuals segment, but in the meantime it decreased for businesses.

Accounts of resident individuals reached approximately 2.94 million, with an annual increase of 4.4%. Even the number of individual accounts, although it has returned to growth, is still far from the maximum level of 3.24 million, which was registered in 2016.

Last year, the number of resident business accounts declined. After reaching an all-time high in 2022, with 239,000 accounts, last year, the number of bank accounts shrank, by 3% less.

The closure of another bank of considerable size, such as Alpha Banka Albania and its merger with OTP Albania, may have had an impact on the total number of business accounts.

While the number of non-resident accounts grew at a high rate last year as well, by 20% more compared to the previous year. Their total number reached more than 60 thousand and non-resident accounts make up about 1.9% of the total number of accounts in Albanian banks. Non-resident accounts are mainly dominated by individuals, with 97% of the total.

Even last year's growth came mainly from individuals, while the number of non-resident business accounts was at levels similar to 2022.

Although the number of bank accounts in Albania is higher compared to the total number of the population, this in itself does not have much meaning to understand the penetration of bank accounts in society. While many Albanians have several bank accounts, a large part of the adult population still does not have one.

In recent analyses, the Bank of Albania estimates that the number of individuals of adult age who own a bank account has reached 70%, from about 40% that this indicator was estimated in 2017. Despite the significant growth in recent years, a a significant part of Albanian adults do not yet own a bank account.

However, recent legal changes are expected to significantly increase the number of Albanians who own a bank account. At the beginning of April, the law "On the account of payments with basic services", which was approved by the Parliament of Albania at the end of 2023, entered into force.

According to the law, the payment account with basic services will be offered to consumers in the Republic of Albania by all banks, regardless of income level, employment status and solvency history. For the holders of this account, banks should offer some basic payment services, without applying fees or against a reasonable fee.

The methodology for calculating the reasonable fee from banks will be determined by a by-law of the Bank of Albania, considering at least the level of national income and the average fees applied by banks for payment services offered in payment accounts.

However, banks must offer all basic payment services with zero fees, for categories that benefit from programs and policies for economic and social assistance schemes, according to the relevant legislation in the Republic of Albania.

This includes unemployment benefit recipients; families and individuals, who are treated with economic assistance; disability payment recipients and their personal assistants; individuals benefiting from invalid status and their personal assistants; blind individuals and their personal assistants; work invalids; orphans; beneficiaries of the funding measure for the child placed in a foster family by court decision; social pension beneficiaries; old age pension beneficiaries; disability beneficiaries, as well as permanent disability pension beneficiaries due to accidents at work and occupational diseases; family pension beneficiaries; beneficiaries of economic assistance for higher education.

The government has warned that pensions will soon be paid into bank accounts, although the terms and methods have not yet been clearly defined.

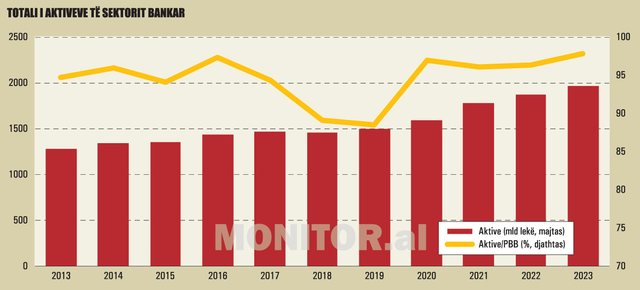

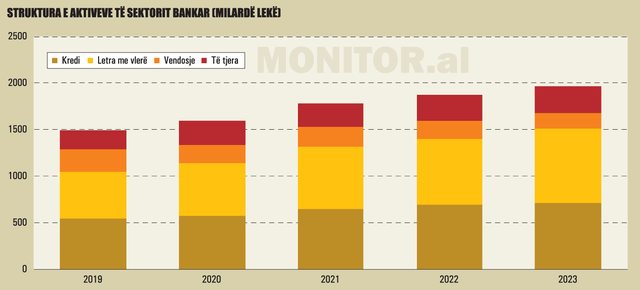

The total assets of the sector reached the value of 1.97 trillion ALL, increasing by 5.1% compared to the previous year. The assets of the sector increased by 5%, despite the added negative statistical effect from the devaluation of foreign currencies in relation to the Lek.

The data according to IFRS show that investments in securities were the largest among the main groups of assets of the banking sector for 2023. According to the figures of the Association of Banks, these investments at the end of last year reached 789 billion ALL, in 11% increase compared to the previous year.

Securities make up 40% of the total assets of the banking sector, up from approximately 38% at the end of 2022. Investments in securities mainly include the debt securities of the Albanian government and foreign public and private issuers.

The increase in the share of securities in the balance sheet seems to have come mainly from the movement of bank funds that were kept in accounts and deposits in other banks.

The value of placements has decreased to ALL 168 billion, 13% more compared to a year ago.

The increase in yields, especially in foreign currency, prompted banks to shift a large part of their funds from deposits to investment in debt securities.

The weight of on-balance sheet placements decreased to 8.5% of total assets, from 10.2% a year ago.

The second largest item in the balance sheet of the banking sector is the loan, for a total portfolio of 718.6 billion ALL, which is 36.5% of the total assets.

The weight of credit on the balance sheet has fallen from the level of 36.9% in 2022, but to a large extent, this has happened due to the effect of the exchange rate.

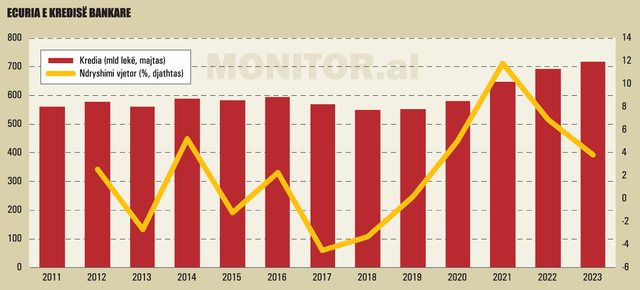

Lending from the banking sector continued to grow in 2023, but growth slowed down for the second year in a row. Statistics of the Association of Banks show that the loan portfolio for the economy at the end of last year reached approximately ALL 719 billion, an increase of 3.9% compared to the previous year.

By 2022, the size of the loan portfolio had almost doubled.

However, the slowdown in growth has been largely influenced by the exchange rate effect. At the end of 2023, the Euro-Lek exchange rate was down by more than 9% compared to the previous year.

This decrease has had a clear negative effect on the loan portfolio in foreign currency, given that approximately half of the loan portfolio of the banking sector is in foreign currency and mainly in Euros.

Data under IFRS do not provide more detailed information on the breakdown of credit, by currency and customer segments. However, according to the standards of the Bank of Albania, the new credit granted by the banking sector for 2023 reached a record value of almost 319 billion ALL, increasing by 14.5% compared to 2022.

Annual new loan growth also improved significantly compared to the previous year's level of 5.3%.

New loan figures should be interpreted with reservations, since they also include refinancing of matured loans, or relocation of existing loans to other banks.

The data show that lending ended last year with surprising performance and growth beyond expectations, amid a slowing economy and higher interest rates.

Experts think that it is precisely the curbing of the increase in interest rates last year that has supported a growth with relatively high credit rates.

The Bank of Albania increased the base rate only twice during 2023 and this indicator remains at the level of 3.25%, among the lowest in Europe and significantly below what is estimated to be the neutral interest rate, which means that interest rates are still at a stimulating territory.

Not coincidentally, the growth of new credit came all in Lek. Last year, the banking sector disbursed 179.7 billion new loans in the local currency, with an increase of almost 35% compared to the previous year. In addition to new lending, Lek loan figures also include a significant amount of foreign currency loans that borrowers decide to convert into local currency, due to the low exchange rate and more favorable interest rates.

According to the main market segments, the new loan marked growth for both private enterprises and individuals.

The new credit for businesses last year reached the value of 217 billion ALL, increasing by 16% compared to 2022.

Loans to individuals also continued to grow and reached an annual value of disbursements of ALL 91.9 billion, an increase of 7.1% compared to 2022.

Measured as portfolio surplus, the annual growth of the total portfolio for businesses was 2.5%, while for individuals, 8.7%. Despite a slowdown in the growth of new loans, the portfolio of individuals continues to have higher rates of annual growth, due to a more stable structure, based especially on long-term loans for housing purchases.

The ratio of bad loans at the end of last year fell to the lowest level in the last 15 years. According to information from the Bank of Albania, the ratio of non-performing loans in December fell to 4.7%, from 5.1% in November and 5% at the end of 2022. This indicator has touched the lowest level since October of 2008.

The performance of non-performing loans last year was significantly better than expected. At the beginning of the year, the projections of the Bank of Albania and commercial banks were oriented towards a slight increase in the ratio of non-performing loans, due to the slowdown in economic growth and the increase in interest rates. But, such a thing did not happen.

Preliminary data from INSTAT showed that the economy grew by 3.44% during 2023 (from 4.8% a year ago), but this did not lead to a deterioration of the bank loan portfolio. Experts believe that the limited effect of the tourism sector on economic growth can also be explained by a rather high degree of informality.

Beyond what official statistics show, the tourism sector is estimated to have had a significant effect on the demand for goods and services and on the health of the private sector of the economy.

It is believed that the small increase in interest rates by the Bank of Albania last year, but also the strengthening of the Lek in the exchange rate, had a significant impact on the decline in the ratio of non-performing loans.

The Bank of Albania raised the base interest rate only twice in 2023 and the level of 3.25% is among the lowest in Europe, far from the rates applied by central banks in Europe and the region. This kept loan yields and interest rates at low levels, even largely correcting the strong growth of late 2022.

Low interest rates also influenced a better-than-expected performance of lending. The expansion of the loan portfolio also helped to reduce the specific weight of the non-performing loan portfolio.

The exchange rate played an important role in maintaining the solvency of borrowers in foreign currency, but with income in Lek. At the end of 2023, the Euro-Lek exchange rate was in annual decline by 9.1%, but in certain periods of the year, the annual decline of the rate reached up to 14%.

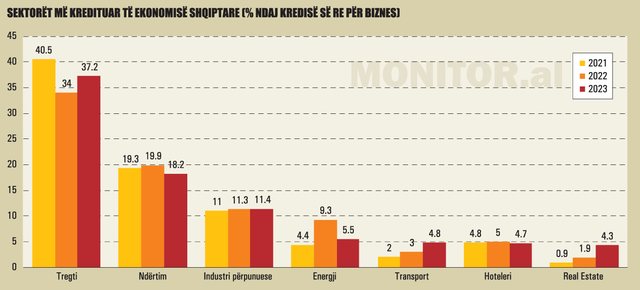

According to statistics from the Bank of Albania, new business loans increased by 16% last year and reached ALL 217 billion. The data shows that, among the sectors with significant weight, the highest growth was recorded by real estate activities, transport and trade.

Trade remains dominant in the structure of credit to the economy, with almost 37% of the total volume of new disbursements. In value, the new credit for trade in 2023 reached 80 billion ALL, increasing by 27% compared to 2022.

Although domestic demand has shown signs of weakness, also due to the significant increase in prices after 2022, the increase in the number of foreign tourists seems to have partially offset this effect.

The second most credited sector of the economy last year was construction, with a new loan value of 39.6 billion ALL, or 18.2% of the total. Construction credit, however, grew at a slower pace, 6.7% more compared to 2022.

Construction credit is experiencing a new cycle of growth, driven by developments in the real estate sector, especially in the capital and the coast.

The increase in property prices in recent years has encouraged the banking system to support investments in this sector, although a part of the portfolio may also be linked to loans for infrastructure investment contracting firms.

The third most credited sector of the economy was the processing industry, with 24.8 billion ALL, or 11.4% of the total. New credit for the manufacturing industry increased by 17% compared to 2022.

The sector of real estate activity marked a high increase in lending, with 164% compared to 2022, and that of transport and storage, with 88% more.

One sector that experienced a significant drop in lending last year was electricity, with 32% less compared to 2022.

The agriculture sector, even last year, recorded lending in modest values, with 2.7 billion ALL in total, with an increase of 5.6% compared to the previous year.

Credit to agriculture is not achieving any significant boost, despite the application of various financing relief schemes and occasional discussions about the need to increase the support of this sector with loans.

According to commercial bank experts, the biggest problems in agricultural lending are related to the lack of guarantees and collateral for loans, lack of information, technical knowledge and management skills of farmers, high fragmentation of land (small farms) and as a result, lack of economies of scale and lack of cooperation between farmers to secure large order contracts, joint use of warehouses, etc.

In general, the new credit data is consistent with the economic trends of recent years, which show an increase in the share of the real estate and services sector in the economy.

The home loan increased for the fourth year in a row in 2023. Bank of Albania data shows that the new home purchase loan reached a new historical record of 48.5 billion alleks, or about 466 million euros. New housing loans increased by 5.2% compared to 2022.

The value of the active portfolio or home loan surplus, at the end of 2022, reached almost ALL 177.2 billion, with annual growth of 6.3%. Growth rates have slowed compared to 2022, but this is partly due to the effect of the exchange rate and the devaluation of the Euro against the Lek.

The relatively low interest rates have caused the home loan to increase, especially in the local currency. The new home loan in Lek, last year, reached 30.2 billion Lek, an increase of 36% compared to the previous year.

Local currency credit accounted for more than 62% of new disbursements for this product.

In total, the banking sector's exposure to real estate loans reached 342 billion ALL, or almost 3.3 billion euros at the end of last year. According to Bank of Albania statistics, the real estate loan portfolio grew by almost 23% during 2023. This figure includes both customer segments, businesses and individuals.

The majority of the portfolio belongs to individuals, with approximately 53% of the total exposure in loans for real estate, while the difference of 47% is loans given to businesses. Currently, real estate loans make up 48% of the total loan portfolio granted to the private sector of the economy.

In recent years, the banking sector has significantly increased the loan portfolio for properties, both for businesses and for individuals. It is estimated that lending has been a very important factor in supporting demand in the real estate market.

Low interest rates have made home loans attractive to borrowers, while at the same time, the cycle of rising real estate prices in recent years has also increased the demand for home loans from households, increasing the perception that buying a property it is a good investment for the future.

The increase in prices has influenced larger values ??of loans taken by individuals to buy apartments, contributing significantly to the increase in the overall volumes of this product.

But, on the other hand, this has also increased the exposure of the banking sector against the performance of the real estate market.

In the vast majority of cases, loans for real estate are secured with properties left as collateral in favor of banks (in the most typical case, the property itself purchased with a loan).

A potential crisis in the real estate market would reduce the value of collateral and expose banks to the risks of loan losses.

In October last year, the Bank of Albania approved the regulation "On data reporting, identification and monitoring of indicators on lending and investments for real estate".

According to the Bank of Albania, this regulation formalizes, standardizes and expands the data collected by banks and lending entities regarding the indicators of the standards they use for exposure to residential and commercial real estate.

Also, the regulation offers the possibility for the Bank of Albania to use these indicators as macroprudential policy instruments, when necessary to mitigate the risks associated with these exposures if they are assessed at high levels.

In the case of residential real estate loans, lending entities must provide the necessary details and data classifications for each such loan in order to identify and monitor indicators of their exposure to the residential real estate market. .

In the last statement of January 2024, the International Monetary Fund (IMF) suggested to the Bank of Albania the establishment of a countercyclical capital increase for the banking sector.

In the statement, the Executive Board of the IMF estimated that the imposition of a countercyclical addition to the capital adequacy ratio for commercial banks could be considered in the medium term, to further strengthen financial stability.

According to statistics from the Bank of Albania, the average interest rate of the loan portfolio for the purchase of housing by individuals in Lek currency, in December last year, was 4.85%. This level is only 0.2 percentage points higher compared to the end of 2022.

Interest rates, especially in the second half of 2023, followed a continuous downward trend, driving significant growth in local currency lending.

The inhibition of the increase in interest rates by the Bank of Albania during the past year affected the correction of the extremely high growth that bond and bond yields had recorded in the second half of 2022.

Yields fell in the first half of 2023, while they were generally stable in the second half, especially for short-term instruments. This had a direct impact on the interest of loans in Lek, which are generally quoted based on the interest of treasury bonds.

The average interest rate of the euro-denominated home loan portfolio reached 5.2% in December 2023, up from 4.44% at the end of 2022.

In the Euro loan, during the past year, a gradual increase in rates was observed, reflecting the monetary tightening of the European Central Bank and the increase of the benchmark indicator, the 12-month Euribor.

The difference between the average interest rate for loans in Euro and those in Lek reached the highest historical level, with 0.35 percentage points more.

However, for borrowers with income in Lek, the increase in Euro interest rates has been balanced by the devaluation of the European currency in the exchange rate. At the end of 2023, the Euro-Lek exchange rate recorded an annual decrease of 9.1%.

Historically, interest rates for loans in Euro have been lower than those in Lek, reflecting especially the lower rates applied by the European Central Bank. But last year, reports changed.

The European Central Bank undertook an aggressive increase in interest rates up to the historical maximum level of 4.5%. The Bank of Albania slowed down the growth and closed the year at the level of 3.25%.

Deposits in the Albanian banking sector increased for the fifth consecutive year in 2023, and the growth rate even improved compared to 2022.

The statistics of the Association of Banks show that at the end of last year, the total value of deposits reached 1.65 trillion ALL, increasing by 5.4% compared to the previous year.

Deposit growth was slightly higher than the 4.9% level a year ago, despite the strong negative effect of the exchange rate on foreign currency deposits.

Data according to IFRS do not provide more detailed information on the structure of deposit growth. However, if we refer to the parallel statistics of the Bank of Albania, the growth of the sector's deposits in 2022 was slightly higher, with 5.7%,

In the segment of individuals, the growth marked the level of 3.2%, while for businesses, the growth was significantly higher, with 15.5% compared to a year ago.

Separated by currencies, growth was slightly higher for Lek, with 6.4% compared to a year ago, foreign currency deposits (reported in Lek) recorded slower growth, with 4.1%. This growth is however significantly reduced by the negative effect of the exchange rate.

If we look at the statistics for Euro deposits (reported without converting to Lek), their growth during 2023 reached 15.9%.

Based on these parallel data, some conclusions can be reached regarding the tendency of deposit growth. This increase has been higher in businesses, reflecting a good sales performance, the positive effects of price increases and, in part, the significant increase in credit for businesses during 2023.

In particular, the high growth of deposits in Euros continues to show an upward trend of foreign currency inflows in the economy, which seems to be related to the increase in income from tourism and services and to the large investment flows of foreign entities in the property market. real estate.

Another factor that may have positively affected the performance of local currency deposits was the fall in government bond yields, which somewhat reduced investors' interest in government debt bonds, following the influx to these instruments that was observed in 2022. , especially in its second half.

The data of the Financial Supervision Authority (AMF) showed that for 2023, the purchases of individuals in the primary market of bonds and bonds reached ALL 37.5 billion, down by 24.5% compared to 2022.

Interest rates on deposits increased marginally for the past year. Bank of Albania statistics show that in December 2023, the average interest rate of new deposits in Lek was 1.64%, from 1.43% at the end of 2022.

The inhibition of interest rate increases by the Bank of Albania and the drop in yields reduced the incentives for the increase of interest on bank deposits for most of last year.

However, interest rates on new deposits increased especially after August and reached the highest annual level in November, at 1.78%.

This can be explained by the stagnation of local currency deposits and the narrowing of the banking sector's liquidity surpluses during most of 2023.

An important role was played especially by the restrictive fiscal policy pursued by the Albanian government. Only after November, with the increase in public spending, bank deposits returned to growth.

The Bank of Albania's monetary policy has helped maintain favorable prices for lending to the economy, but on the other hand, it has not provided many incentives to increase savings and benefits from them.

A similar growth rate of deposit interest rates last year was also recorded for the Euro currency. According to the Bank of Albania, the average interest rate for new Euro deposits in December was 0.99%, from 0.71% at the end of 2022.

The increase in interest on deposits in Euro has not followed much the pace of the increase in interest rates on deposits in the European markets. In the Albanian market, monitoring the movements of the ECB's monetary policy has been quite limited.

This can be explained by the high supply of funds in Euro and the lack of financial investment alternatives in this currency. Deposits in the European currency grew by more than 6% last year.

Also, the low interest rates of Euro deposits are also related to the regulatory policies of the Bank of Albania. The central bank does not pay banks remuneration for the forced reserve in this currency, except that it requires a higher level of this reserve, compared to the Lek.

This increases the intermediation costs in Euro for the banking sector and directly affects the maintenance of lower interest rates for deposits.

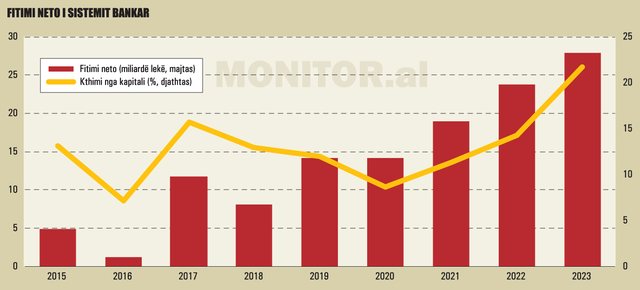

According to preliminary data published by the Albanian Association of Banks, the joint profit of commercial banks with the International Financial Reporting Standards (IFRS) reached ALL 27.9 billion, the highest ever recorded.

The profit of the system has increased by 17%, compared to 2022.

The increase in the profits of the banking sector came mainly from the increase in interest rates in foreign currency and from the further decrease in the ratio of problem loans, despite the most pessimistic forecasts for 2023.

The European Central Bank continued with the aggressive increase in interest rates during 2023 and this was reflected in the interest rates of the international markets and in higher returns from the sector's foreign currency assets.

This includes, of course, loans in Euros, which are mostly granted with variable interest rates, based on the progress of the Euribor (usually the 12-month one).

The increase in Euribor during the past year also brought an increase in interest income, although the effect of the exchange rate partially consumed this increase, expressed in Lek.

The data so far according to IFRS are not detailed at the level of separate items of income and expenses, but nevertheless some general conclusions can be drawn, analyzing the data based on the parallel reporting standards of the Bank of Albania.

According to local standards, in 2022, the banking sector achieved a net profit of ALL 32.5 billion, an increase of almost 50% compared to the previous year.

The sector registered a significant increase in net interest income, a fact that proves that the cycle of increasing interest rates has had a significant positive effect on banks' balance sheets. Net interest income (interest income minus interest expenses) reached ALL 69.5 billion, with an annual increase of 28%.

Non-interest income has also recorded a high increase to ALL 18.6 billion, an increase of 41% compared to a year ago. The increase came mainly as a result of the improvement of the result from financial instruments.

For 2022, this result had been negative, due to the rapid increase in yields, while during 2023 it returned to positive territory.

Meanwhile, expenses for provisions (according to local standards) increased significantly by 153%, but they remained at a low absolute value, around ALL 3.8 billion, making the effect of their increase on the financial result to be limited.

The increase in the financial result has been clearly reflected in the profitability indicators of the banking sector. Average net return on equity for 2023 reached 21.67%, up from 14.25% a year ago.

The improvement in the return on capital came mainly from the increase in profits, but also from some dividend distributions carried out by certain banks last year.

The distribution of dividends has slowed down the growth of shareholder capital and has had a positive effect on the return on capital. While the average net return on assets increased to 1.4%, from 1.3% a year ago.

Euroization of credit for the economy fell significantly last year. According to the figures of the Bank of Albania, at the end of 2023, foreign currency loans accounted for 47.1% of the total portfolio of the banking sector.

Compared to a year ago, the share of loans in foreign currency has decreased by almost five percentage points.

This also marks the largest decrease in the share of foreign currency loans in the space of one year, since the launch of the deeuroization strategy by the Bank of Albania in 2017.

The indicator of loans in foreign currency, in relation to total loans, has marked a decrease for most of the banks of the system, with the exception of two of them. Compared to the end of December 2016, this indicator has decreased for 10 of the 11 banks of the system.

The surplus of foreign currency loans not hedged by the exchange rate, where Euro loans account for about 91%, has marked a further decrease in the share of total foreign currency loans. At the end of December 2023, these loans accounted for 25.7% of foreign currency loans, or 12% of total loans.

In absolute terms, there is an 8.6% decrease in unhedged loans against the exchange rate, compared to the end of 2022. However, the Bank of Albania emphasizes that this significant decrease also reflects some structural changes in classification by a small number of banks, this is related to the internal strategy of the banks.

Loans exposed to exchange rate risk, that is, cases where the borrower's income is in a currency different from the currency of the loan, are those with

higher risk profile. For this reason, this indicator carries a special importance in monitoring the measures to reduce Euroization.

At the end of the second half of 2023, the indicator that measures the weight of foreign currency deposits to total deposits, reached 54.3%. The ratio decreased by 0.7 percentage points compared to the previous year.

The distribution according to banks of the share of deposits in foreign currency fluctuates between the levels of 47.15% and 59.52%. It turns out that 10 of the 11 banks operating in the banking system register a value of this indicator above 50%, which potentially makes them subject to the mandatory reserve rate of 20%.

The indicators monitored by the Bank of Albania are reported stripped of the effect of fluctuations in the exchange rate of the national currency against major foreign currencies.

In the periodic analysis of the progress of the indicators, which are the object of the de-euroization strategy, the Bank of Albania estimates that these indicators have moved in the right direction to achieve the objectives targeted by the measures to reduce the euroization, although the size of the change is relatively small .

According to the Bank of Albania, this development highlights the need to maintain a long-term focus on evaluating the effects of measures to reduce euroization and the variety of economic and social factors that can affect the performance of the selected indicators.

In the second half of 2023, the appreciation of the Lek against the main currencies was significant and faster than in previous periods.

However, even when corrected for this exchange rate performance, the performance of the indicators monitored to assess the effects of the de-euroization measures has generally been in line with the intended objectives.

"The structural changes in the economy over the last few years, where the strong increase in tourism income and inflationary developments are singled out, have been accompanied by changes in economic and monetary policies, as well as in the behavior of agents of the real economy. For these reasons, distinguishing the effects closely related to de-euroization measures remains a difficult process.

However, these measures have an inhibitory effect on the progress of euroization and in their absence, the size of the movement of any of the indicators, or even its direction, would be different" - says the analysis of the Bank of Albania.

In 2017, the Bank of Albania signed a memorandum with the Ministry of Finance and the Financial Supervisory Authority, with the aim of expanding the use of the national currency in the financial system and the Albanian economy.

Until now, only the Bank of Albania has taken concrete regulatory measures, which tend to increase the use of the local currency in the banking sector.

These measures tend to increase the costs of financial intermediation in foreign currency and at the same time decrease them for the Lek./ Monitor.al

Sot, më 4 maj 2024, në tregun valutor, dollari amerika...

The foreign exchange reserve suffered a slight decline...

Today, May 3, 2024, in the foreign exchange market, th...

The euro exchange rate touched a new historic low today. ...

Banorët e Tiranës dhe ato të Sarandës kanë barrën më të la...

The demand for loans in the banking sector increased in th...

Today, May 2, 2024, in the foreign exchange market, the Am...

Furrat e bukës dhe pastiçeritë për rreth 2 javë, përka...

12-month bond yields fell slightly at the last auction in ...

Today, on May 1, 2024, in the foreign exchange market, the...

A kilogram of imported cereals in March 2024 cost at least...

Environmental problems are increasing all over the wor...

Today, on April 30, 2024, in the foreign exchange market, ...

The Non-Life insurance market has shown a more balanced di...

There are about 29,000 free professionals practicing their...

The Albanian government has requested another loan from th...

Today, on April 29, 2024, in the foreign exchange market, ...

Today, on April 28, 2024, in the foreign exchange market, ...

It's almost 11:00. After a not-so-comfortable journey, on ...

Today, on April 27, 2024, in the foreign exchange mark...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

A road accident occurred this evening on Nikolla Zoraqi St...

Three people were shot and wounded in Elbasan last night b...

A serious incident occurred this Tuesday in the Yrshek are...

An accident occurred this Tuesday on "Dituria" street in K...

All of Southern Europe will face changing weather conditio...

Albania was hit by temperatures significantly higher than ...

For the first time, Pogradec welcomed the Inter-Lake Chess...

Albania has achieved a record for the employment of foreig...

US Secretary of State Marco Rubio arrived in Manila on Jul...

In the space of a few days, Ukrainian President Volodymyr ...

The spokesman for the Iranian Foreign Ministry warned Bulg...

Autoritetet italiane sekuestruan pako me afër 800 kilogram...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

Construction company licenses will have a validity period ...

The Centralized Purchasing Operator recently opened a tend...

The new draft law "On the Bank of Albania" provides that t...

This Tuesday, one US dollar is bought for 81.2 lek and sol...