Paradoxically, Albania is among the countries with the best economic performance, but poverty is increasing

Albania is turning out to be one of the countries with...

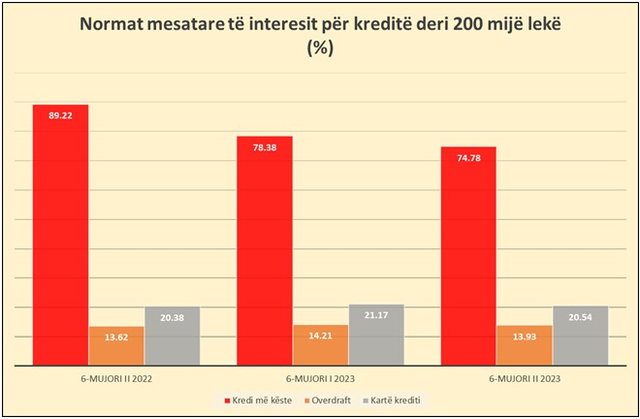

Average interest rates for consumer loans in the financial market fell further in the second half of last year.

According to data from the Bank of Albania, the average effective interest rate for loans up to 200 thousand ALL decreased to 74.78%, from 78.38% in the previous six months and 89.22% in the second half of last year. .

Whereas, for bank advances (overdrafts) up to 200 thousand ALL, the average effective rate decreased to 13.93%, from 14.21% that was in the first half of the year, but increased from the level of 13.62% that was in the second half of 2022 .

Even for credit cards with a limit of up to ALL 200,000, the average interest rate fell to 20.54%, from 21.17% in the first half of the year, but a slight increase from the level of 20.38% in the second half of of 2022.

For installment loans worth from 200,000 to 600,000 ALL, the average effective interest rate increased to 30.45%, from 24.57% in the first half of the year.

Meanwhile, for large loans from 600 thousand to 2 million ALL, the average interest rate decreased to 11.68%, from 12.95% in the first six months.

The above interest rates are calculated on all consumer loans granted by banks and non-bank financial institutions, based on the actual data that are reflected in the Credit Register administered by the central bank. The calculation of the average effective interest rate serves as the basis for further calculating the maximum effective interest rate for consumer loans (maximum NEI)

The average effective interest rate does not mean only the nominal interest rate of the loan, but all costs charged to the customer for the loan, including commissions or other fees.

The decrease of the effective average interest rate despite an increasing trend of nominal rates in the last two years can be explained by an increasing competition in the consumer loan market and especially for smaller loans.

Given that here the margins are relatively high, lending institutions have had room to compete with prices, despite the fact that the cost of providing funds has started to increase after 2022.

The application of a maximum effective interest rate by the Bank of Albania seems to have served as a factor that moved the average loan interest down. Since the beginning of 2022, when the application of the ceiling interest rate began, this indicator has continuously moved downward for small loans with installments of up to 200 thousand ALL./ Monitor.al

Albania is turning out to be one of the countries with...

Today, on January 23, 2024, the US dollar is bought at 94....

The 10-year bond auction that took place on Monday confirm...

Today, on January 22, 2024, the US dollar is bought at 94....

Albania should apply legal changes to the deposit insuranc...

Until now, the amount of stock created by the non-exportat...

The Association of Builders of Albania predicts for th...

Sot më 21 janar 2024, dollari amerikan blihet me 94.7 ...

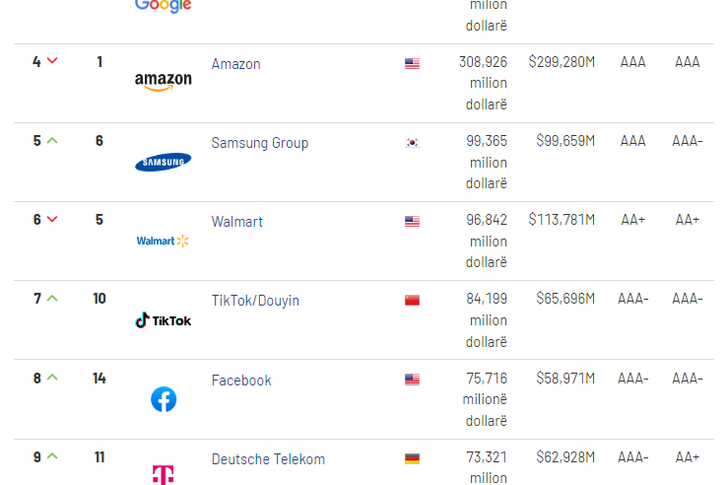

Brand Finance has listed the most important companies and ...

Sot më 20 janar 2024, dollari amerikan blihet me 94.7 ...

The increase in the stock of state guarantees that have be...

Today, January 19, 2024, the US dollar is bought at 95...

Sot më 18 janar 2024, dollari amerikan blihet me 95 le...

Core inflation closed down last year. According to dat...

Today, January 17, 2023, the US dollar is bought at 94.9 A...

Drejtoria e Përgjithshme e Tatimeve ka publikuar të dh...

The directive of the Ministry of Finance and Economy f...

The Municipality of Vaut i Deja announced that it has ...

When asked how satisfied they are with life, Albanians...

Today, January 16, 2024, the US dollar is bought at 94...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

New details have emerged from the serious accident that oc...

A serious accident occurred this Wednesday on the Elbasan-...

Citizen MH, 61, a fisherman, was found dead near the islan...

Another phase of the international operation, codenamed "T...

The Institute of Geosciences has shared a forecast for wea...

Rising energy and fertilizer prices are expected to contin...

Over 18,000 foreign citizens from 140 countries have appli...

This Wednesday, our country will be under the influence of...

Prime Minister Andy Burnham has announced that most bus fa...

France's parliament has passed a law to ban social media f...

US Secretary of State Marco Rubio arrived in Manila on Jul...

In the space of a few days, Ukrainian President Volodymyr ...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

Businesses will no longer be required to simply register t...

Despite economic growth and income in recent years, Albani...

This Wednesday, one US dollar is bought for 81.4 lek and s...

Construction company licenses will have a validity period ...