Territorial Reform/ Berisha warns Rama: We will get Albania back on its feet

DP leader Sali Berisha has spoken about extending the dead...

DP leader Sali Berisha has spoken about extending the dead...

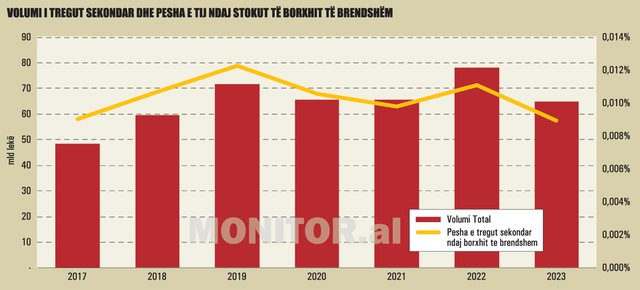

The secondary market of bonds and bonds of the Albanian government remains small and the efforts to develop it, so far, have not yielded significant results. The Bank of Albania considers the market illiquid, with a low number of transactions and volumes, where banks are generally the main players in this market.

According to the information from the Bank of Albania, the volumes in the secondary securities market last year reached 64.9 billion ALL, a value that represents about 9% of the total domestic debt stock. The trading volume during 2023 results in a decrease from the previous year, to about 17%.

The Bank of Albania estimates that this turnover level is a clear indicator that the secondary market in Albania is far from being developed. For comparison, countries with a developed secondary market report their own trading volume 10-30 times higher than the debt stock.

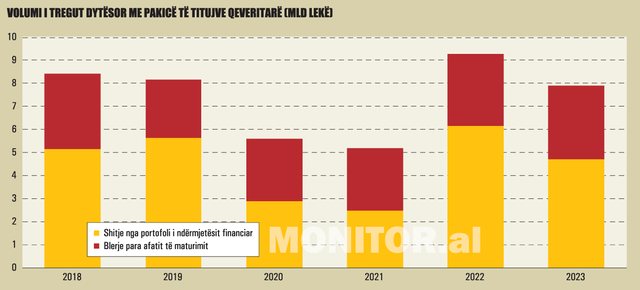

The secondary retail market of government bonds last year was worth 7.9 billion lek, or about 76 million euros. This market segment refers to the purchase and sale transactions that natural and legal persons perform with licensed financial intermediaries, mainly commercial banks.

The figure includes both sales of securities by individuals and businesses before maturity to financial intermediaries, as well as reverse transactions, purchases by individuals and entities of government securities held in the portfolio of financial intermediaries.

According to data from the Financial Supervision Authority, for the past year, the volume of the secondary retail market decreased by 15% compared to 2022. The decrease in secondary trading volumes seems to be related to the significant decrease in yields during the year of past, after the strong growth they had recorded in the second half of 2022. This caused individuals and businesses to invest less in bonds and bonds, both in the primary and secondary markets.

The majority of secondary retail trading volumes are sales from the financial intermediary's portfolio (when the individual or business buys securities from banks/commissioning companies).

These transactions accounted for 60% of the total volume of secondary retail trading last year. However, their value fell by 23% compared to 2022, mainly due to the drop in yields.

In general, individuals and commercial companies in Albania continue to make their investments in the government securities market mainly in the primary market. Last year, the value of purchases in the secondary market was ALL 4.73 billion, while purchases in the primary market (through direct participation in auctions) reached ALL 40.1 billion.

Meanwhile, transactions of securities sales before maturity by individuals and businesses last year were worth 3.16 billion ALL, at levels close to 2022. In fact, in periods of declining yields, the sale of securities before maturity may be more profitable because it implies a higher price against their face value.

The non-increase in the value of trading in the conditions when the yields suffered a significant decrease can also be an indicator of the poor development of the market and little knowledge of its mechanisms by small investors.

Securities are traded through financial intermediaries (commissioning companies) licensed by the AMF, which are mostly commercial banks. In general, financial intermediaries do not charge commissions for the purchase and sale of securities in the retail market.

The customer pays only the price of the security quoted by the bank which may be higher (at a premium) or lower (at a discount) than the nominal value, depending on the performance of yields in the market. Income from securities yields is classified as investment income and is taxed at source at the rate of 15%.

The same thing happens with the premium over the selling price. In case an individual or business sells the bond/bond before maturity, at a price higher than the purchase price, the difference between them (additional income) is taxed as investment profit, at the rate of 15%.

In a statement for "Monitor" magazine, the Bank of Albania estimates that there are a number of reasons why the secondary market is underdeveloped.

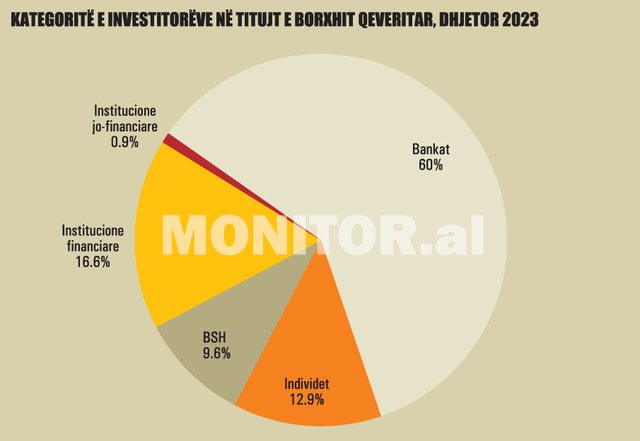

The investor base in the securities market is small, domestic, highly concentrated and with similar preferences for liquidity. The main holders of domestic debt are the banks, which own about 70% of the total stock. A significant part of the debt is owned by individuals, who are almost entirely Albanian citizens.

Although holdings of financial institutions such as investment funds, pension funds, insurance companies, including deposit insurance, have increased in recent years, their holdings remain low, constituting about 16% of the stock of internal debt.

According to the Bank of Albania, it is generally this segment of the financial market which is seen as a promoter in the development of the capital market, exploring trading opportunities, expectations on interest rates and allocation to different financial assets.

Meanwhile, non-resident, institutional or retail investors are almost non-existent and with sporadic participation in the domestic government securities market.

The Bank of Albania estimates that their access to the internal market would offer a high commitment of foreign funds, with an impact on reducing risk premiums and flattening the yield curve, as well as financial expertise in trading and increasing the liquidity of secondary market.

On the other hand, this market segment acts on an opportunistic basis, being unfaithful and risk-averse, if there are uncertainties about the country's credit risk or those of interest rates and exchange rates.

The fact that this type of investor is very sensitive to risks requires, as a precondition for commitment, the minimization of risks through the existence of a liquid secondary market, to exit the investment with low cost, developed payment system and low legal risks.

Another factor, according to the Central Bank, is that there is a lack of genuine investment banks in Albania, with a focus on intermediation of financial products of interest rates, money market, shares or their derivatives.

Given the high transaction costs in the secondary market, and the high financial costs of maintaining a skilled staff and adequate infrastructure for trading securities in the secondary market, banks generally prefer a "hold-to-maturity" strategy and rarely engage in secondary market transactions when they see a financial opportunity or driven by the need for liquidity.

Prof. Dr. Elvin Meka, Dean at the Faculty of Business and Law, Tirana Business University, thinks that the modest development of the secondary market of government securities is a function of many historical, institutional, economic, regulatory and social and psychological factors, to take all together have conditioned a very anemic development of this market over the years.

"As far as historical factors are concerned, the secondary market of government bonds has its beginnings no further than 1995, when for the first time the Bank of Albania started efforts to develop this market near commercial banks, with the aim of attracting individuals and enterprises to this market, in addition to their participation in the primary market.

Further, the market would take another dimension with the beginning of open market operations, even by the Bank of Albania, through the instrument of Repurchase Agreements (REPO) in 1998, which in any case was only its beginning.

Meanwhile, it would be the Department of the Tirana Stock Exchange, as early as May 1996, that would carry out the first transactions in the secondary market of government securities, with the trading of a 5-year bond between the Bank of Albania and the Savings Bank, as well as in continuing with the trading of treasury bonds among its member commercial banks.

The Tirana Stock Exchange, as a department of the Bank of Albania, would be the first pioneer in the realization of official trading of transactions in the secondary market of government securities.

Then, the market would know other developments, related to the sale and purchase of these securities with full rights between banks, as well as the expansion of the retail market of these securities, between institutions and individuals, but still in very modest volumes compared to the primary market, as well as in a very limited number of transactions per year", he says.

From the institutional point of view, according to him, the Albanian financial market has always been a very shallow market with limited volumes of transactions.

"This has come not only because of the absolute dominance of this market by commercial banks, but also the almost total lack of non-bank financial intermediaries in this market, for business and regulatory reasons.

On the other hand, the Albanian financial market has lacked, almost all the time, other investment alternatives in titles and securities, from the private sector, turning government titles into the only investment alternative in the financial market, both for banks and institutions , as well as for individuals.

On the other hand, this lack of alternatives and the structural problem that the banking sector in Albania has had since 1992, i.e. the marked imbalance between deposits and loans (where the volume of deposits has always exceeded at least 1.7 times the total of loans) has conditioned banks to very rarely use the secondary market of government securities, maximizing their investments in the primary market of these securities.

It should not be forgotten that the first private title was traded on the Albanian title market only in 2023", says Mr. Mecca.

He thinks that the regulatory aspect of the securities market in Albania has historically favored banks in financial mediation in this market, either from the point of view of the organization of this mediation, or from its regulatory point of view.

"Practically, even the current legislation blocks from a practical point of view any type of enterprise, which is not a bank, to enter the market of government securities, but also the secondary market of securities in general.

Legislation has favored and continues to favor commercial banks, in order to provide almost monopoly positions in mediation in the secondary securities market, while this creates a paradoxical situation, since commercial banks, by their nature of business, are fundamentally interested in to attract customers who bring deposits to the bank and not to seek services that do not bring funds to their coffers, or worse, to offer services and products that take customers' deposits away from the bank.

In such conditions, with this legislation that Albania has, technically it cannot be expected that there will be promotion and development of the secondary market of titles, whether they are governmental or private", - notes Mr. Meka.

Finally, but no less important, in this shallowness of the government securities market, according to him, are the social and psychological factors related to the Albanian individual, as an investor and customer of this market.

"For objective and historical reasons, but also for the permanent lack of investment alternatives, apart from bank deposits, which have been known since the 20s in Albania, Albanian individuals and investors have massively invested in bank deposits and much less in government titles.

Despite the strong growth of public (individual) investments in government securities, especially in recent years, the level of financial education, but also many psychological factors have conditioned their minimal participation in this market.

Moreover, the Albanian public remains massively uninformed about the functioning of the secondary market, meanwhile, being a monopoly market by the banks, the brokerage fees are completely discouraging for an expanded use of the secondary market, which is used by the public more in emergency situations, rather than financial management of their investments", he says.

The very poor development of the secondary market poses problems for an optimal functioning of the financial market, primarily in determining a fair price of financial securities at any time.

According to the Bank of Albania, the lack of a liquid secondary market, where the prices of securities are determined freely and frequently, undermines the reliability of the yield curve, which would serve as a source of accounting valuation for portfolios that various investors such as banks or financial institutions report to interested parties.

The lack of reliable secondary market prices makes it difficult for the market to steer the pricing of new issues in the primary market, significantly increases the risk of the liquidity premium, and weakens the signals that monetary policy receives from a reliable yield curve. of the government on the market's expectation on interest rates.

Therefore, the Bank of Albania assesses that the efforts to develop the secondary market should be comprehensive, as the beneficiaries are all actors such as the government, banks, central bank and other strategic investors such as investment funds, etc.

The higher liquidity of the secondary market can allow investors to increase the duration of their portfolio, achieve higher returns, while bringing about a flattening of the yield curve, and in this sense, reducing the cost of government borrowing.

In 2018, the Ministry of Finance, in cooperation with the Bank of Albania and five commercial banks in the country, started the implementation of the reference securities project.

The five commercial banks participating in the project were committed to take the role of market makers, with the continuous quotation of the reference titles, according to certain defined criteria related to the minimum quoted volume and the maximum difference between the purchase price and the sale, in exchange for the privilege granted by the Ministry of Finance for exclusive participation in the primary auctions of reference titles for their purchase for personal needs, or for their clients.

Currently, the list of reference securities includes fixed coupon bonds with 3-year, 4-year and 5-year maturities.

In the analysis of the Bank of Albania, for a period of 2 years from the start of the project, the secondary market of government securities and that of reference securities marked a satisfactory progressive growth, where both improvements in trading volumes and improvements in absorption of these instruments in the primary market with improved coverage ratios and high participation of client orders mediated by market maker banks.

Also, a high dynamism was observed between the signals issued by the secondary market and the results of the auctions in the primary market, but subsequent developments have dictated a decrease in the dynamism of the secondary trading of the reference securities in particular and the secondary market in general. However, gradually the effect of this project seems to have been fading.

Events such as the November 2019 earthquake following the pandemic situation dictated high government borrowing needs in the domestic market and not only in subsequent years, exhausting to a significant extent the demand in the primary market and leaving low spaces in increasing demand in the secondary market.

The pandemic, on the other hand, led to movement restrictions and reduced staffing of financial intermediaries and, in this regard, to low incentives and a drop in trading volumes. Also, the merger process of several banks during the last years is thought to be another factor in reducing the number of transactions in the secondary market of government bonds.

According to the Bank of Albania, with the decrease in the number of banks, the potential for the rotation of market-making banks from other banks decreases, in the case of a system that evaluates with points and replaces the weakest booster with another bank aspiring to be a market maker .

Based on the data of the Ministry of Finance, for the year 2023, the total value of the secondary trading of the reference securities was about ALL 7.9 billion, increasing by 59% compared to the previous year. However, measured as a share of the secondary market, actions with reference securities constitute about 12% of its total volume.

In the view of the Bank of Albania, a key factor for the development of the government securities market, including the secondary one, would be the expansion of the investor base. Expanding the investor base is mostly related to how capable the government and regulatory authorities are in increasing credibility and creating a positive and attractive investment environment.

In recent years, regulatory authorities have undertaken legal improvements to draft a new capital market law; improvements in the direction of the payment system for the issuance and repayment of securities and the electronic registration of debt holders, unique identification with an international ISIN number, which is expected to serve both in increasing the confidence of non-resident investors and in connecting the central depository of securities issued in the domestic market with international ones.

Finally, the Bank of Albania, in cooperation with the AMF and the Ministry of Finance and Economy, is taking the necessary steps to start an important project with the EBRD, through which the needs for changes in the legal acts that regulate the activity in financial markets, with the aim of making the trading environment safer, both for foreign and domestic investors.

Regardless of the above, the Bank of Albania assesses that banks in their intermediary function should further increase efforts to expand clients through the provision of counseling, lower financial costs of services and financial education.

Also, it is necessary for banks or other market actors to focus more on the development of the secondary market, through the exploration of profitable opportunities from taking positions based on the expectation of interest rates/yields for a defined time horizon , not being simply an investor of funds, but also their administrator, based on the perceived risks of interest rates and credit.

The expert of financial markets, Elvin Meka, thinks that, in order for the secondary market to be deepened and developed further, it was necessary first of all to redimension the legal framework, which should open the market for competition.

"Currently and technically, the secondary market remains a monopoly of commercial banks, which have no incentive to develop such a market, as it goes against their nature of business.

If, under the name of Albania's integration into the EU, the legislation that regulates the functioning of the securities market will continue to remain so, due to the lack of participation of institutions and enterprises other than banks, then Albania will have to wait a long time until a inherent development of this market.

At a minimum, regulators may consider easing the rules for participating as intermediaries in this secondary market of non-bank financial institutions, which are currently supervised and licensed by both the Bank of Albania and the AMF.

This would allow market opening and greater opportunities for competition and competitive and low intermediation fees for individuals and market participants. Without competition, the development of this market cannot be hoped for," says Mr. Meka.

According to him, the legislation should enable the activation of this market through the Albanian Stock Exchange - ALSE, which would enable not only higher institutional visibility for the market, but would also attract more investors and market participants, interested in offered mediation services through the platform of ALSE./ Monitor.al

Journalist Ola Xama, in a post on social networks, has...

The expansion of the daily rental sector, driven by th...

Today, on February 17, 2024, in the foreign exchange m...

The year 2023 can be described as a good hydro year where ...

Rritja e ulët e produktivitetit, efektet e plakjes së popu...

Social and health insurances come first in the hierarc...

Today, on February 16, 2024, in the foreign exchange m...

Pagesat me kartë bankare regjistruan përsëri një rritj...

Detyrimet e papaguara të bizneseve dhe individëve ndaj adm...

Today, on February 15, 2024, in the foreign exchange m...

As after two years, inflation has suffered the stronge...

Today, on February 14, 2024, in the foreign exchange m...

Olive oil during the past year could actually be considere...

The pace of price increases eased in January as inflation ...

Employment in the banking sector reached an all-time high ...

Sot, më 13 shkurt 2024, në tregun valutor dollari amerikan...

CNA has opened a survey where it seeks to know the attitud...

The increase in the number of domestic and foreign tou...

Albania is the only country in the region that does no...

Today, February 12, 2024, in the foreign exchange mark...

CNA has launched another investigation that could lead to ...

Irfan Hysenbelliu is a businessman that we call "Irfan the...

In March 2026, CNA launched another investigation centered...

The arrested mayor of Tirana, Erion Veliaj, with 13 charge...

The Special Board of Appeal (KPA) decided this Monday ...

The KPA vetting decided this Thursday to dismiss the p...

Suela Salavaçi, a prosecutor in the Prosecutor's Offic...

The Special Board of Appeal reinstated the prosecutor ...

Citizen MH, 61, a fisherman, was found dead near the islan...

Another phase of the international operation, codenamed "T...

Police have arrested a 34-year-old woman at Rinas Airport ...

A serious accident has occurred on the Lezhë-Shëngjin axis...

This Wednesday, our country will be under the influence of...

All of Southern Europe will face changing weather conditio...

Albania was hit by temperatures significantly higher than ...

For the first time, Pogradec welcomed the Inter-Lake Chess...

Prime Minister Andy Burnham has announced that most bus fa...

France's parliament has passed a law to ban social media f...

US Secretary of State Marco Rubio arrived in Manila on Jul...

In the space of a few days, Ukrainian President Volodymyr ...

At a time when industrial products are increasingly taking...

Trust among people is not just a three-syllable word. It c...

Master of humor Todi Llupi has passed away at the age of 7...

The ninth edition of "MIK Festival" kicked off with one of...

Businesses will no longer be required to simply register t...

Despite economic growth and income in recent years, Albani...

This Wednesday, one US dollar is bought for 81.4 lek and s...

Construction company licenses will have a validity period ...